Rare Earth Industry Update Predicts Continued Supply Strain

1. ALTERNATIVE ENERGY 8 FEBRUARY 2011

RARE EARTH INDUSTRY UPDATE Matt Gowing, CFA 416.860.8675

mgowing@mackieresearch.com

Raveel Afzaal, Associate 416.860.7666

2011 Rare Earth Industry Update: We Remain Bullish

We are pleased to present a comprehensive rare earths industry update. This forward-looking report predicts future demand and supply of rare

earths and analyzes the impact of changes in supply-demand dynamics on rare earth prices. The key findings of our report suggest that supply

of rare earths, particularly heavy rare earths, is expected to remain strained over the next four years.

Inelastic demand in high-growth industries

• Rare earths are an integral input, with little or no substitutes, required in a multitude of industries.

• The average CAGR of these industries range from 6% to 15%.

• Rare earths are usually a small component of the overall manufacturing costs of the end products in most industries. Therefore,

companies are more likely to be able to bear an increase in rare earth prices compared to an increase in prices of raw materials that

constitute a large component of the overall manufacturing costs.

Supply to remain strained

• In this report, we detail a list of new rare earth mines that are expected to come on-line over the next five years (see Figure 7a). We

believe the supply of rare earths is going to remain strained, even after incorporating a very generous assumption that these new rare

earth mines will come on-line on schedule and meet their production goals.

• China consumes more than 60% of its current rare earth production. We expect its domestic consumption to further increase based on

its significant investments in domestic industries that require rare earths, such as wind turbines. In addition, China is no longer

interested in realizing lower margins through the sale of unrefined rare earths. It aims to build vertical industries to further participate

in the down-stream business and realize higher margins. Therefore, we do not expect China to flood the global markets with cheap rare

earths in the foreseeable future.

Rare earth prices to further increase, given tight supply and inelastic demand in high-growth industries

• Many of the light rare earths, such as

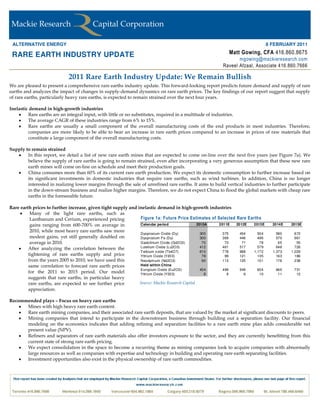

Lanthanum and Cerium, experienced pricing Figure 1a: Future Price Estimates of Selected Rare Earths

gains ranging from 600-700% on average in Calendar period 2010A 2011E 2012E 2013E 2014E 2015E

2010, while most heavy rare earths saw more

Dysprosium Oxide (Dy) 305 375 454 504 580 672

modest gains, yet still generally doubled on Dysprosium Fe (Dy) 300 369 446 496 570 661

average in 2010. Gadolinium Oxide (Gd2O3) 70 73 71 78 65 55

After analyzing the correlation between the Lutetium Oxide (Lu2O3) 412 461 517 579 648 726

•

Terbium oxide (Tb4O7) 610 778 968 1,172 1,373 1,029

tightening of rare earths supply and price Yttrium Oxide (Y203) 78 99 121 135 163 186

from the years 2005 to 2010, we have used this Neodym ium (Nd2O3) 90 113 125 151 176 238

same correlation to forecast rare earth prices Held within China

Europium Oxide (Eu2O3) 454 499 549 604 665 731

for the 2011 to 2015 period. Our model Yttrium Oxide (Y203) 8 8 9 10 11 12

suggests that rare earths, in particular heavy

rare earths, are expected to see further price Source: Mackie Research Capital

appreciation.

Recommended plays – Focus on heavy rare earths

• Mines with high heavy rare earth content.

• Rare earth mining companies, and their associated rare earth deposits, that are valued by the market at significant discounts to peers.

• Mining companies that intend to participate in the downstream business through building out a separation facility. Our financial

modeling on the economics indicates that adding refining and separation facilities to a rare earth mine plan adds considerable net

present value (NPV).

• Refiners and separators of rare earth materials also offer investors exposure to the sector, and they are currently benefitting from this

current state of strong rare earth pricing.

• We expect consolidation in the space to become a recurring theme as mining companies look to acquire companies with abnormally

large resources as well as companies with expertise and technology in building and operating rare earth separating facilities.

• Investment opportunities also exist in the physical ownership of rare earth commodities.

2. Page 2

TABLE OF CONTENTS

Industry Overview ................................................................................................................................................................... 3

Supply & Demand ................................................................................................................................................................... 4

Rare Earths Pricing Forecast ................................................................................................................................................. 12

Consolidation ......................................................................................................................................................................... 14

Conclusion .............................................................................................................................................................................. 15

Appendix 1 – Rare Earth Industry News ........................................................................................................................... 16

Appendix 2 – Rare Earth Mineral Profiles ....................................................................................................................18-23

Appendix 3 – Selected Company Profiles:

Avalon Rare Minerals Inc. (AVL-TSX, Unrated) ...................................................................................... 24

Neo Material Technologies Inc. (NEM-TSX:, BUY/TARGET PRICE: $10.00) ...................................... 25

Relevant Disclosures/Analyst Certification ...................................................................................................................... 26

www.mackieresearch.com

3. Page 3

INDUSTRY OVERVIEW

WHAT ARE RARE EARTHS?

Rare earth elements (REE), also described as rare earth oxides (REO), are a group of 17 metals critical to several clean energy, clean-tech, and

electronic applications. Of these 17 elements, the group of lanthanides amount to 15. They are listed in Figure 1b. A group of chemically similar

elements, the lanthanides, are grouped together on the chemical periodic table.

Distinguishing between heavy rare earths and light rare earths: In Figure 1b, we separate the 15 lanthanides into light rare earths elements

(LREE) on the left side, and heavy rare earths elements (HREE) on the right. The rare earths are defined as those chemical elements beginning at

number 57, lanthanum, on the periodic table and running consecutively through to number 71, lutetium. The chemical differences in rare earths

come about due to differences in ionic radius, crystal structure, and basicity of the mineral. For example, Neodymium magnets hold their

magnetic properties much better due to their internal crystal structure. The ionic radius of the heavy rare earths is smaller than the light rare

earths, which makes them denser, more resistant to high temperatures, and less reactive in some circumstances. The rare earths vary in crustal

abundance with from cerium, at 60 ppm (parts per million) to thulium and lutetium, at 0.5 ppm. The division is important as HREEs command

higher selling prices and therefore higher margins for their producers.

Yttrium - Some call it the 16th lanthanide: Yttrium is often found along with other lanthanides in nature. Although it has similar chemical

properties, it is not officially classified as a lanthanide.

Scandium, atomic number 21: Scandium rounds out the group of 17 rare earth elements. It typically occurs in rare earth ores, in minor amounts,

because of its smaller atomic size.

Figure 1b: The 15 Lanthanide Elements

LREE (Light Rare Earth Elements): HREE (Heavy Rare Earth Elements):

Element # in periodic table: Element # in periodic table:

.

57 La lanthanum 63 Eu europium

58 Ce cerium 64 Gd gadolinium

59 Pr praseodymium 65 Tb terbium

60 Nd neodymium 66 Dy dysprosium

61 Pm promethium 67 Ho holmium

62 Sm samarium 68 Er erbium

69 Tm thulium

70 Yb ytterbium

71 Lu lutetium

Source: USGS, Mackie Research Capital

INDUSTRIAL USES

Rare earths are an essential ingredient used in a multitude of industries: The market for rare earths has grown rapidly given their use in a

wide array of applications. In some applications, rare earths do not have any effective substitutes and are vital to the manufacturing process.

The highest rare earths-consuming industrial applications are shown in Figure 2.

www.mackieresearch.com

4. Page 4

Figure 2: End-Market & Applications of Rare Earths

Rare Earths are a group of elements with unique properties

Rare Earth Elements Catalytic Magnetic Electrical Chemical Optical

Lanthanum (La) X X X X

Cerium (Ce) X X X X

Praseodymium (Pr) X X X X

Neodymium (Nd) X X X X

Samarium (Sm) X

Europium (Eu) X

Gadolinium (Gd) X X

Terbium (Tb) X X

Dysprosium (Dy) X X

Holmium (Ho) X

Erbium (Er) X

Ytterbium (Yb) X

Yttrium (Y) X

Source: Lynas Corp

SUPPLY & DEMAND

CONSUMPTION

Volume growth outlook for rare earths usage is high: In Figure 3, we provide a forward-looking comparison by usage for various rare earths

consumption growth rates as forecast by two leading industry specialists, Roskill and IMCOA (Industrial Minerals Company of Australia).

Demand for rare earths is expected to increase from 95,000 tonnes in 2005 to about 180,000 tonnes in 2014. What is striking is the general

expectation for high growth rates across all categories. In certain end-markets, i.e., those products that require terbium and dysprosium, such as

magnets, growth rates are expected to sustain double-digit increases, even approaching 15%. Additionally, almost all of the end-markets are

expected to experience average estimated growth ranging from 8% to 11%.

Figure 3: Projected Growth of End Markets

% of % of % of 9-yr 08-14 11-14

Applications Elements 2005 Supply 2008F Supply 2014F Supply CAGR Growth Growth

Magnets Dy*, Nd, Pr, Sm, Tb* 17,150 18.0% 26500 21.4% 39-43,000 22.8% 10.2% 7.5% 10-15%

Metal alloys Ce, La, Nd, Pr 7,200 7.6% 22500 18.1% 43-47,000 25.0% 22.6% 12.2% 15-20%

Catalysts Ce, Nd, La 21,230 22.3% 23000 18.5% 28-30,000 16.1% 3.5% 3.9% 6-8%

Polishing Ce, La, Pr 15,150 15.9% 15000 12.1% 19-21,000 11.1% 3.1% 4.9% 6-8%

Glass Ce, Er*, Gd*, La, Nd, Yb* 13,590 14.3% 12500 10.1% 12-13,000 6.9% -0.9% 0.0% 0-1%

Phosphors & pigmentsEu*, Tb*, Y* 4,007 4.2% 9000 7.3% 11-13,000 6.7% 13.0% 4.9% 7-10%

Ceramics 0.0% 7000 5.6% 8-10,000 5.0% - 4.3% 7-9%

Other 16,935 17.8% 8500 6.9% 10-12,000 6.1% -4.7% 4.4% 7-9%

Total 95,262 100% 124,000 100% 170-190,000 100% 7.3% 6.4% 8-11%

Elements with *: HREE

Source: Roskill, IMCOA

www.mackieresearch.com

5. Page 5

RARE EARTHS SUPPLY INADEQUATE TO MEET DEMAND

Shortfall particularly severe for the heavy rare earths: Avalon’s Thor Lake project and Quest’s Strange Lake projects currently have two of the

largest deposits of heavy rare earths in the world. Our research suggests that heavy rare earths are likely to experience the greatest shortages. As

shown in Figure 4, according to IMCOA, terbium and dysprosium are expected to have global shortages of 105 and 500 tonnes, respectively, by

2015. This implies that the future supply of terbium and dysprosium would only be able to meet 80% and 73% of their respective demands in

2015.

Figure 4: Supply vs Demand in 2015

Source: IMCOA

According to China’s Ministry of Commerce, there is a concern that at today’s rates, China’s heavy rare earths supply could be depleted in the

next 15-20 years. Even though the heavy rare earths are sold in much smaller volumes than neodymium and the lighter elements, shortfalls in

supply would be a major driver for relative price outperformance of the heavy rare earths.

New mines coming on-line have a higher mix of light as opposed to heavy rare earths: The supply impact of new mines coming on-line may

have little effect on reducing the upward pressure on rare earths prices, especially heavy rare earths prices. The two non-Chinese projects

expected to come on-line in the next two years, Mt. Weld in Australia and Mountain Pass in the US, are weighted towards light rare earths.

Moreover, 72% of Lynas Corp’s Mt Weld deposit is composed of lanthanum and cerium (light rare earths). Figure 5 further supports our

argument that heavy rare earth content (HREE) as a percentage of the total rare earth from existing and future mines is quite low.

Consequently, HREE will likely be much scarcer going forward.

www.mackieresearch.com

6. Page 6

Figure 5: HREE Content as a Percentage of Total Rare Earths by Mine

Resource TREO HREE

(million Grade (million Content

Deposit tonnes) (% TREO) tonnes) (% TREO) Cut-off Grade

Bayan Obo, China 1,460 3.9% 56 2% n/a

Kvanefjeld, Greenland 215 1.0% 2.6 14% 0.015% U3O8

Mountain Pass, USA 20 9.2% 1.8 1% 5% REO

Nechalacho, Canada 65 2.1% 1.3 20% 1.6% REO

Mt. Weld, Australia 12 9.7% 1.2 3% 2.5% REO

Nolans, Australia 30 2.8% 0.9 4% 1.2% REO

Dong Pao, Vietnam 11 6.9% 0.8 n/a 6.9% REO

Bear Lodge, USA 9 4.1% 0.4 n/a 1.5% REO

Hoidas Lake, Canada 2 2.6% 0.04 7% 1.5% REO

Source: IFRI Energy Breakfast Roundtable, Christian Hocquard

Figure 6 reinforces the point that even with new mines coming on-line, the supply of heavy rare earths is expected to remain tight. Mt. Weld in

Australia is expected to begin producing at a rate of 20,000 tonnes per year in 2011. Molycorp’s Mountain Pass project in the United States, and

possibly Alkane Resources Limited’s Dubbo project may come on-line by end of 2012 and 2014, respectively. Avalon’s Thor Lake mine in

Canada is expected to come online in 2015.

Mt. Weld is expected to add 19 tonnes of terbium and 34 tonnes of dysprosium at initial production. Mountain Pass is expected to add only trace

amounts of terbium and dysprosium when it comes on-line. Nolan’s Bore is expected to add 16 and 68 tonnes of terbium and dysprosium,

respectively. Moreover, Thor Lake is expected to add an additional 45 tonnes of terbium and 250 tonnes of dysprosium.

Figure 6: Rare Earth Content by Mine for 2012-2014

Source: IMCOA

www.mackieresearch.com

7. Page 7

Figure 7a: Rare Earth Mines Development Outside of China

Potential

Project Location Owner Production

Mount Weld Australia/Malaysia Lynas Corporation Ltd mid 2011

Mountain Pass USA Molycorp Minerals, RCF, Goldman Sachs and Traxys mid 2012

Nolans Australia Arafura Resources Ltd. 2013

Dubbo Zirconia Australia Alkane Resources Ltd. 2014

Thor Lake Canada Avalon Rare Metals Inc. 2015

Bear Lake USA Rare Element Resources Ltd 2015

Hoidas Lake Canada Great Westerns Minerals Group 2015+

Kvanefjeld Greenland Greenland Minerals & Energy Ltd. 2015/2016

Strange Lake Canada Quest Rare Minerals Ltd. 2016

Source: IMCOA

Unexpected supply shocks may occur as delays are encountered in new mine development: When these projects do come online, they are not

expected to produce an adequate quantity of heavy rare earths to satisfy demand. Typical mining risks accompany these projects and delays

may be commonplace in reaching operating status by the expected dates. Even if these projects meet scheduled timelines, supply for heavy rare

earths over the next three to four years will continue to be tight. We believe this shortage will be further exacerbated by China restricting

supplies to the rest of the world.

Figure 7b provides a comparison of some of these projects in terms of current valuation, heavy rare earth content, and historical price

performance.

Figure 7b.Rare Earth Mining Companies Comparable Table

Mkt Cap/

Measured Measured Measured Measured Measured Mkt Cap/

& & & & Total Mkt Cap/ and Total

Inferred Indicated Inferred Indicated Inferred Indicated Inferred Indicated Mineral Inferred Indicated Inventory

Resource Resource Reserve Grade Grade Grade Grade Inventory Inventory TREO Pre-Tax Resources Resources Value

Ticker (mt, 000s) (mt, 000s) (mt, 000s) (TREO) (TREO) (TREO) (TREO) (mt, 000s) (mt, 000s) (mt, 000s) IRR ($/tonne) ($/tonne) ($/ tonnes)

Lynas Corp - Mt. Weld LYC-AU 5,294 12,200 2,040 8.30% 7.96% 8.30% 7.96% 439 971 1,410 6,698 3,032 2,087

Molycorp - Mt. Pass MCP-US - - 48,375 7.00% 7.00% - - 3,386 n/a n/a 1,256

Alkane Resources - Dubbo Zirconia ALK-AU 35,700 37,500 - 0.90% 0.90% 0.90% 0.90% 321 338 659 899 856 439

Arafura Resources - Nolans ARU-AU 12,800 17,400 - 2.60% 2.92% 2.60% 2.92% 333 508 840 18% 1,469 963 582

Great Western Minerals - Hoidas Lake GWG-V 287 2,561 - 2.14% 2.43% 2.14% 2.43% 6 62 68 65,219 6,428 5,851

Greenland Minerals & Energy Ltd. - Kvanefjeld GGG-AU 92,000 365,000 - 1.01% 1.01% 1.01% 1.01% 929 3,687 4,616 24% 416 105 84

Avalon Rare Metals Inc - Thor Lake AVL-T 226,880 88,130 12,001 1.30% 1.53% 1.30% 1.53% 2,949 1,348 4,298 23%** 209 457 143

Rare Element Resources - Bear Lodge RES-V 15,876 - - 3.46% 3.46% 549 - 549 40%*** 1,101 n/a 1,101

Quest Rare Minerals Ltd - Strange Lake QRM-V 114,823 - - 1.00% 1.00% 1,148 - 1,148 36% 316 n/a 316

Frontier Rare Earths FRO-T 20,810 22,920 - 1.99% 2.32% 1.99% 2.32% 414 532 946 671 523 294

** Avalon's IRR estimate based on Mackie Research model. IRR estimate for the remaining companies based on company announcements.

*** Rare Element Resources IRR estimate is after-tax.

Source: Companies, Mackie Research Capital

www.mackieresearch.com

8. Page 8

Figure 7c.Rare Earth Mining Companies Share Price Performance

Price Change (%)

Company Ticker 1 Month 3 Months 6 Months 1 Year

Lynas Corp LYC-AU -5 40 111 236

Molycorp MCP-US -6 44 288 -

Alkane Resources ALK-AU 18 41 180 280

Arafura Resources - Nolans ARU-AU -5 8 78 82

Great Western Minerals GWG-V 83 159 444 293

Greenland Minerals & Energy Ltd. GGG-AU 1 32 189 114

Avalon Rare Metals Inc - Thor Lake AVL-TSX -2 64 148 182

Rare Element Resources RES-TSXV -3 31 380 334

Quest Rare Minerals Ltd QRM-TSXV 11 32 117 135

Frontier Rare Earths FRO-TSX -8 - - -

Pele Mountain Resources Inc GEM-TSX -10 80 341 120

Quantum Rare Earths Development Corp QRE-TSX 2 6 113 34

Ucore Rare Metals Inc. UCU-TSX 24 78 138 172

Commerce Resources Corp. CCE-TSX -9 27 202 135

Rare Earth Metals Inc RA-TSX -5 -8 44 -32

Stans Energy Corp RUU-TSX 169 264 1131 841

Dacha Strategic Metals DSM-TSXV -7 -6 7 -20

Neo Material Technologies Inc NEM-TSX 14 54 113 112

Neo Materials (NEM – TSX, BUY Recommendation, $10.00 price target)

Source: Bloomberg

China in supply restriction mode: In 1992, China began selling rare earths at a significant cost discount to producers outside of China. Chinese

miners were able to produce rare earths at lower costs due to weak environmental regulations and cheap labour. This led to rare earth mines

outside of China closing down. China continued to invest in rare earth production and now supplies 97% of the market globally. However, the

country is currently in a unique position; domestic demand for rare earths in China has increased dramatically. As well, a substantial increase in

demand has occurred in the export market.

China intends to create vertical industries that not only mine rare earth ore, but also consist of world-leading refining and processing facilities.

The priorities of job creation and production dominance are factors that are likely to result in China continuing to place increasing restrictions

on rare earths exports. As well, China has been imposing increasingly stringent environmental regulations that place further supply pressure on

the output from rare earth mines.

China has taken a multi-pronged approach in restricting supplies: As discussed, China has been making its export restrictions increasingly

stringent. We expect this trend to continue, providing further upward pressure on rare earth prices.

Export Tariffs – In 2006, China introduced a flat 10% export tariff across all rare earths. In 2008, this was revised to 15% for light rare earths

and 25% for heavy rare earths. On December 16, 2010, the Chinese Ministry of Finance announced that it will raise export taxes for some

light rare earth elements − such as cerium, lanthanum, and neodymium − to 25% in 2011.

Export Quotas – In 2003, China started introducing export quotas that have continued to become increasingly stringent and further restrict

supplies of rare earths in the export markets. Export quotas for 2010 totaled 30,258 tonnes compared with 50,145 tonnes in 2009,

representing a 40% decline. On December 28, 2010, China announced allocations of rare earths quotas of 14,446 tonnes for H1/2011,

equivalent to a 35% decline relative to H1/2010. This became a major catalyst for stocks exposed to rare earths prices. We believe the

upcoming July quota allocation announcement could again act as a major catalyst for higher prices.

Elimination of the Value-Added Tax (VAT) Rebate - In 1985, China began to implement an export tax rebate policy that has since been in

steady decline. In 2004, the export tax rebate for rare earth metals was reduced to 5% from 17%. In May 2005, the export tax rebates for all

rare earths were abolished.

www.mackieresearch.com

9. Page 9

Production quotas – In order to prevent over-mining and illegal mining, the authorities introduced product quotas in 2007. As of

September 2010, the production quotas stood at 82,320 tonnes.

Figure 8: Chinese Rare Earths Quotas Continue to Decline

(Metric Tonnes) 2008 09/1H 09/2H 2009 10/1H 10/2H 2010 11/1H

Foreign 8,211 6,685 10,160 16,845 5,978 1,768 7,746 3,746

Local 34,156 15,043 18,257 33,300 16,304 6,208 22,512 10,762

TOTAL 42,367 21,728 28,417 50,145 22,282 7,976 30,258 14,508

Y/Y % Change

Foreign 105% -11% -83% -54% -37%

Local -3% 8% -66% -32% -34%

TOTAL 18% 3% -72% -40% -35%

Source: Chinese Commerce Ministry, Mackie Research

TREND OF POLITICAL DEVELO PMENTS SUGGEST RARE EARTHS SUPPLY REM AINS TIGHT

Even if the Chinese government were to announce that full-year 2011 quotas will be flat compared to the 2010 level, we believe there is a strong

likelihood of further near-term increases in rare earths pricing. Again, this is due to the tight state of rare earths supply-demand. We have

included a number of recent comments from noteworthy sources regarding Chinese export policy on rare earths in Appendix 1. The key take-

away is that China is expected to reduce export quotas in 2011, or at-least keep quotas at a consistent level from 2010.

PRICING TRENDS INDICATE FURTHER INCREASES

Rare earths have experienced strong pricing gains over a multi-year period. Not surprisingly, the supply squeeze has helped sustain these

pricing gains. Also interesting is that price gains have recently accelerated. Pricing of terbium and dysprosium has been particularly strong over

the past several months (Figure 9).

Figure 9: Historical Prices of Rare Earths

(US $/KG) 2005 2006 2007 2008 2009 Q1/2010* Q2/2010* Q3/2010* Q4/2010* 2010**

Product (oxide)

Dysprosium 35 70 89 118 116 190 200 293 305 305

Dysprosium Metal 70 89 118 150 250 290 282 300 300

Terbium 300 460 590 721 362 600 515 628 610 610

Gadolinium - - 10 10 7 9 9 61 70 70

Yttrium - 5 11 13 15.5 20 20 63 78 78

Europium 290 240 324 482 493 530 530 600 640 640

Lutetium 550 550 412 412 412

Neodymium 6 14.8 28.9 27.21 15.29 30 30 60 90 90

Held within China

Europium 290 240 324 482 493 423 416 454 454 454

Yttrium - 5 11 13 15.5 7.57 7.11 7.57 7.57 7.57

* end of quarter prices

** estimated current price as of 30th December 2010

Source: IMCOA, metal-pages.com, Lynas, Martin van Britsom & Diksmuide, Asian Metals

Figure 10 illustrates rare earths data points spanning the past few decades. We note the severe price correction as a result of the 2008/2009

global recession and the recent reversal to price improvement. The figure also provides a good overview of the magnitude of cyclical price

swings in the rare earths market. Currently, we are experiencing the upswing of pricing strength, and if the trend continues, our pricing

estimates may be surpassed (see Figure 11).

www.mackieresearch.com

10. Page 10

Figure 10: Historical Prices of Rare Earths (US$/kg)

Data Source: http://minerals.usgs.gov/minerals/pubs/commodity/rare_earths/mcs-2010-raree.pdf

Figure Source: http://tikalon.com/blog/blog.php?article=RE_shortage

DEM AND

Rare Earths – Substantial Market Opportunity: According to the China Rare Earth Information Center, the global rare earths market amounted to

about 124,500 metric tonnes in 2008. In 2009, as a result of the recession, volumes dropped to roughly 100,000 tonnes. The market is currently in

the process of a drastic recovery in sales volumes, and is believed to have jumped back to about 135,000 tonnes in 2010, and expected to increase

to about 152,000 tonnes in 2011. By 2014, IMCOA (Industrial Minerals Company of Australia) estimates the rare earths market will exceed $2

billion in value. Data obtained from Metal Pages and Roskill support the contention that rare earths sales represent a market opportunity in the

billions of dollars. Figure 11 illustrates that in 2007, neodymium was the largest segment of the rare earths market by value, closely followed by

cerium.

Figure 11: Historical Rare Earths Oxide (REO) Pricing 2007 Production Value - $1.05 Bln

Source: metal-pages.com, Martin van Britsom & Diksmuide, Tianjiao International

www.mackieresearch.com

11. Page 11

Figure 12 depicts the steady growth of total global production. Given a higher current production run-rate combined with recent strength in

pricing, we believe the value of this market has grown significantly in the past couple of years and will continue to do so.

Figure 12: Historical Rare Earths Oxide (REO) Production

Source: metal-pages.com, Martin van Britsom & Diksmuide, Tianjiao International

Outlook for demand strong, driven by clean-tech and “new age” applications: Figure 13 provides a segmented list characterizing the

downstream end-markets that have been driving a considerable amount of the demand for rare earth materials. The appearance of electric

vehicles and renewable technologies on this list is a reminder of the key role that green and renewable technologies play in the industry. Growth

of miniaturized electronics is believed to be considerable, another key demand driver for rare earths.

Figure 13: Projected Growth of Downstream End-Markets & Applications

Unit Shipments (000s)

End Use 2008 2014 CAGR REE Used

Computers 293,000 529,000 12.50% Nd, Pr, Sm, Tb, Dy

Electric bicycle motors 23,000 100,000 34.20% Nd, Pr, Sm, Tb, Dy

Electric vehicle batteries 527 2,717 38.80% La, Ce, Pr, Nd

Electric vehicle motors 527 2,717 38.80% Nd, Pr, Sm, Tb, Dy

LCD displays 102,200 375,000 29.70% Eu, Y, Tb, La, Ce

Moblie CE 1,055 58,000 122.90% Nd, Pr, Sm, Tb, Dy

Mobile phones 1,222,245 2,250,000 13.00% Nd, Pr, Sm, Tb, Dy

Wind turbines 81 239 24.10% Nd, Pr, Sm, Tb, Dy

Source: metal-pages.com, Martin van Britsom & Diksmuide, Tianjiao International

www.mackieresearch.com

12. Page 12

RARE EARTHS PRICING FORECAST

We have forecasted and analyzed supply and demand imbalances for each of the relevant rare earth elements using our proprietary

methodology in order to derive our rare earth price estimates. The future demand projections for each element are based on Roskill’s projected

CAGR for the specific industries that use the respective rare earths in their manufacturing processes. The US Department of Energy’s estimates

are used to determine individual rare earth content in existing and upcoming mines. This, coupled with industry expert consensus regarding the

commercial operations start date of the new mines, allows us predict future supply of individual rare earths on a year-to-year basis. We then

analyze the relationship between historical demand and supply imbalances and the price for each of the rare earths under consideration. After

analyzing the correlation between excess demand and price for the years 2005 to 2010, we have used this same correlation to forecast rare earth

prices for the 2011 to 2015 period. For each element, this is done by calculating the average change in price per one tonne increase in excess

demand (where excess demand equals global supply less global demand per element).

In the terbium tear sheet in Appendix 2, for example, we calculate a historical average price of $7/tonne for years 2006-2010. This average ratio

of $7/tonne is projected forward, and is multiplied by our proprietary estimates for change in excess demand. These calculations are repeated for

each element and are detailed in Appendix 2. The end-result of our price forecasts are shown in Figure 14.

Figure 14: Rare Earth Price Forecasts (US$/kg)

Calendar period 2010A 2011E 2012E 2013E 2014E 2015E

Dysprosium Oxide (Dy) 305 375 454 504 580 672

Dysprosium Fe (Dy) 300 369 446 496 570 661

Gadolinium Oxide (Gd2O3) 70 73 71 78 65 55

Lutetium Oxide (Lu2O3) 412 461 517 579 648 726

Terbium oxide (Tb4O7) 610 778 968 1,172 1,373 1,029

Yttrium Oxide (Y203) 78 99 121 135 163 186

Neodymium (Nd2O3) 90 113 125 151 176 238

Held within China

Europium Oxide (Eu2O3) 454 499 549 604 665 731

Yttrium Oxide (Y203) 8 8 9 10 11 12

Source: metal-pages.com, IMCOA, Roskill, US Department of Energy, Mackie Research Capital

Appendix 2 contains summaries of the supply and demand projections we use to derive our rare earth element price estimates. Also in

Appendix 2 we include a one-page table from the US Department of Energy’s December 2010 report, ”Critical Materials Strategy” featuring

tables that provide an overview of the supply-demand dynamics for each element.

RECENT EVENTS INCREASE PRO SPECTS OF FURTHER PRICE STRENGTH

On January 24, 2011, Molycorp announced it would be targeting production of 40,000 tonnes per annum (tpa) at mine start-up, double its

previous rate. This was an important announcement because Molycorp’s Mountain Pass mine, after Lynas’s Mt. Weld project, represents the

industry’s next new capacity addition to the market. We believe this announcement further highlights the global shortage of rare earth supplies

and increased interest by investors in the space. Our analysis indicates that this mine will add only trace amounts of heavy rare earths compared

to Avalon, which has significant heavy rare earth resources.

China’s December 28 rare earth export quota reduction set off a flurry in the rare earth stock prices. China decreased H1-2011 quotas by 35%

YOY, which led to sharp increases in the share prices of rare earth companies outside of China. We do not believe these restrictive export quotas

are a short-term phenomenon. China currently consumes about 60% of rare earths domestically and its future consumption is expected to

increase significantly. There are concerns that by 2015, China may not be able to meet even its own internal demand for rare earths.

www.mackieresearch.com

13. Page 13

Chinese government nationalized 11 rare earth mines. In the third week of January 2011, China nationalized 11 rare earth mines in the eastern

province of Jiangxi. China took this step to protect the dwindling supply of heavy rare earths as these mines are rich in heavy rare earths. This

move also helps curb illegal and irresponsible mining practices in the region that had led to environmental damage. We believe nationalization

will provide further upward pressure to the prices of rare earths, particularly heavy rare earths, as the state strengthens its control over the

mines. This bodes well for Avalon, which has a heavy concentration of heavy rare earths at its Thor Lake project. A comprehensive summary of

rare earth-related industry events is shown in Appendix 1.

CONSOLIDATION

EXPECTED TO BECOM E A RECURRING THEM E IN THE RARE EARTHS SPACE

In order to unlock the full potential of the mines and realize higher margins, the companies will need to participate in the downstream business.

We believe the rare earth mining companies realize that the risk-return profile of their respective projects is more attractive with equity partners

that share the huge costs associated with building the mine and the additional costs involved with building out separation facility. For instance,

Avalon expects to spend over $1 billion in capital expenditure to develop its mine and an additional $300 million to build out its separation

facility. We have already seen a rise in bankable off-take agreements and believe this to be a segue to consolidation in the industry through

M&A activities.

Figure 15: TREO Basket Price by Mine

Operator Arafura Rare Element Quest Rare Frontier Rare

Avalon Lynas Corp Molycorp Resources Resources Minerals Earths

Weighted Average Price/KG Nechalacho Mt Weld Mountain Pass Nolans Bear Lodge Strange Lake Frontier/ZC1

Europium 2.6 2.3 0.6 2.1 2.9 1.1 3.2

Gadolinium 2.2 0.6 0.1 0.6 0.7 1.6 0.9

Terbium 3.4 0.5 0.0 0.5 1.1 3.8 1.1

Dysprosium 8.1 0.4 0.0 1.0 1.2 12.3 2.3

Holmium 3.6 0.0 0.0 0.0 0.2 6.8 1.0

Erbium 2.1 0.0 0.0 0.0 0.1 4.6 0.5

Thulium 4.3 0.0 0.0 0.0 0.0 12.5 1.0

Ytterbium 4.5 0.0 0.0 0.0 0.1 13.1 1.0

Yttrium 10.5 0.3 0.1 1.2 0.7 25.3 3.7

Lutetium 0.6 0.0 0.0 0.0 0.0 1.6 0.1

0.0 0.0 0.0 0.0 0.0 0.0 0.0

Lanthanum 9.3 15.0 19.6 11.7 18.4 7.8 15.0

Cerium 22.1 28.9 30.5 29.5 29.3 17.0 27.4

Praseodymium 3.0 3.5 2.9 3.8 2.7 2.0 3.0

Neodymium 16.0 16.6 10.8 19.1 10.7 9.6 14.2

Samarium 1.4 0.8 0.3 0.8 0.8 0.9 0.8

Price/KG 93.9 68.8 64.9 70.4 69.1 119.9 75.1

Source: Companies, Mackie Research Capital

We have analyzed the characteristics of Avalon’s Total Rare Earth Oxide (TREO) basket and found that its current market price is approximately

$90/kg (Figure 15). However, in its pre-feasibility report, the company assumes it will realize a TREO price of about $22/kg. If it builds a

separation facility and further refines the rare earths, we believe the company has the potential to realize a much higher TREO price ($35-

$50/kg) and improve the economics of its projects (from 12% IRR to mid 20%s IRR). We estimate the capital expenditure required to build a

separation facility that processes $25,000 tonnes will be more than $300 million.

A highly active off-take market has developed for advanced rare earth projects. Over the past two months, we have seen increased activity in

the off-take market for rare earths, primarily driven by concern amongst end users.

www.mackieresearch.com

14. Page 14

Figure 16: Comparable Off-take Agreements

Date Supplier Off-taker Price ($ mm)

5/11/2010 Molycorp W.R. Grace (U.S. Chemical Producer) undisclosed

24/11/2010 Lynas Corporation Sojitz Corporation (A Japanese Trading House) 250

12/10/2010 Molycorp Sumitomo Corp 130

Source: Mackie Research Capital

In November 2010, Molycorp agreed to sell more than 75% of its lanthanum production each year to WR Grace & Co over five years. Financial

terms for the agreement were not disclosed. In November 2010, Lynas signed an agreement with a Japanese trading house. The agreement

entails Lynas starting shipments of 1,000 to 3,000 tonnes of rare earths near the end of 2011, and increasing shipments to 9,000+ tonnes per year

by 2013. The contract price reflects the spot market price at the time of delivery plus shipping costs. Furthermore, Molycorp signed a seven-year

off-take agreement with Sumitomo Corporation in December 2010. The agreement calls for shipment of about 2,500 metric tonnes per year of

cerium- and lanthanum-based products and 250 tonnes per year of didymium oxide (which is a mixture of neodymium and praseodymium). In

return, Sumitomo agreed to purchase shares in Molycorp for a total consideration of $100 million as well as provide $30 million in cheap debt

financing.

Off-take agreements a natural path to consolidation. We expect to see an increase in M&A activities involving mining companies with

significant deposits of heavy rare earth content or those mining companies that are expected to come on-line in the near term. The list of logical

suitors is long, with many major Japanese electronic companies at the top of that list.

Molycorp (MCP-US) is currently in discussions with Neo Materials (NEM-TSX, BUY recommendation, $10.00 price target) to send rare

earths to China. In return, Neo would help Molycorp make rare-earth alloys and metals in Thailand. Molycorp has been very clear regarding its

goal to become a mine-to-magnets integrated firm. Neo Materials, conversely, has monopoly over the US magnets industry and possesses strong

expertise in building and operating rare earth separation facilities. We believe M&A activity involving these two companies will deliver

synergies and be a significant driver of value for both companies. It would demonstrate to Neo’s investors that it has reliable future supply of

key manufacturing inputs, which shows longevity and continuation of Neo’s proven business model. Furthermore, it would allow Neo to

diversify its supply exposure away from China to expand its export business, despite the increasingly stringent Chinese export policies. In

addition, Neo’s unparallel expertise in building and operating separation plant facilities would be a significant value add if Molycorp decides to

go ahead with its plans to build a separation facility. It may also help Molycorp share the financial burden of building out its mine and

separation facility with a reliable off-take partner. We believe this is the right time for Molycorp to look at such ventures. The all-time high

prices of rare earths and the shrinking supply put the company in the position to negotiate favourable terms for the off-take agreements.

We expect to see similar discussion of consolidation in the industry as other rare earth mining companies near production. We expect China,

which is the world’s largest consumer of rare earths, to play a major role in the consolidation of the industry. China bought all or part of 184

foreign mining assets for $37.2 billion in 2008 according to Ernst & Young, while the rest of the world was struggling with the onset of the

recession. It is our understanding that China has in the past approached companies like Molycorp and Lynas regarding potential takeover bids.

We expect China to continue to look for opportunities to improve its resource asset base to feed its growing economy.

www.mackieresearch.com

15. Page 15

CONCLUSION

WE REM AIN BULLISH O N RARE EARTHS, BUT TAKE CARE WHEN “PICKING YOUR SPOTS”

In 2010, investors did not require a considerable amount of “craftiness” in selecting which rare earth companies to add to their portfolios. A

tremendous number of equities that were associated to the rare earth sector experienced considerable gains. This experience is not surprising

when considering the price performances of the underlying rare earth elements highlighted in this report. As we progress through 2011, we

remain bullish on the sector. However, investors will require a more discerning investing approach going forward. Some of our key

recommendations and observations include:

• Focus on the “heavies”. This applies not only to the rare earth mining plays, but the other rare earth investment opportunities that

exist in the sector; including those “arbitrage” plays that own and hold physical rare earth elements.

• Brace yourself for consolidation. As the rare earth cycle progresses, we believe those companies with global leading expertise in

“manipulating rare earth molecules” may look more attractive in the eyes of senior mining companies bringing projects to the

operating stage. Other strategic investors may also become attracted to ownership of these technologies. Our industry sources suggest

that negotiations are gaining traction in this regard.

• Look for continued rare earth pricing strength in 2011, but less drastic export quota reductions from the Chinese government.

While 2011 will likely not show us the severe cuts in export quotas in the same order of magnitude from the Chinese government as

we saw in 2010, the international supply-demand situation should remain tight. Heightened geo-political tensions over global access

to China’s “strategic” source of rare earths may provide further upward pressure on prices.

We are very excited about what is to come from the rare earth sector in 2011. Yes, rare earth price swings have historically proven to exhibit

severe cyclicality. However, we believe rare earths are currently in the robust phase of their cycle, and take exception to any view that “the rare

earth price bubble that is about to burst”. However, investors will certainly have to be more discerning with respect to their investment strategy

in the sector in 2011. We believe that taking into account the key points in this report should help in the quest for outperformance in what

remains an exciting space.

www.mackieresearch.com

16. Page 16

APPENDIX 1

SUMM ARY OF POLITICAL ANNOUNCEMENTS/EVENTS RELATING TO CHINESE RARE EARTH EXPORT QUOTAS

Date Source Comment

China is building strategic reserves in rare-earth metals. The reports say storage facilities built in recent months in the

07-Feb-11 Wall Street Journal Chinese province of Inner Mongolia can hold more than the 39,813 metric tons China exported last year.

Chinese Society of China’s chief rare earths research body says it expects the nation to become a net importer, even though it is the world’s

04-Feb-11 biggest producer.

Rare Earths

China’s Ministry

20-Jan-11 of Land & The Ministry of Land and Resources, invoked a seldom used mining law to take direct control of 11 rare earth mining

Resources districts in southern China.

China's Ministry of China cut its export quotas for rare earths by 35% in the first round of permits for 2011 relative to H1/2010, threatening

30-Dec-10 to extend a global shortage of the minerals needed for wind turbine, electric cars and other clean tech applications.

Commerce

China's Ministry of China will raise the export taxes for some elements to 25% next year. The move is an increase from the 15% temporary

16-Dec-10 export tax on neodymium. Lanthanum and cerium, were not taxed in 2010, and will be taxed at 25% in 2011.

Finance

Japan's Trade China, the world’s largest producer of rare-earth metals, will speed up exports of the minerals after delays disrupted

15-Nov-10 supply, according to Japan’s Trade Minister Akihiro Ohata.

Minister

China has to strictly manage the exports and make dynamic adjustments, without hampering development of the

world’s high- tech industries,” said Chen Zhanheng, the head of research at the society, which represents the nation’s

Chinese Society of major producers. “China should dedicate itself to develop high-tech end products, rather than shipping out low value-

11-Nov-10

Rare Earths added raw materials,” Chen said yesterday in an interview in Hong Kong at a rare earth conference. “The idea to swap

mineral resources for advanced technologies never works.”

China will reduce its rare earth export quotas next year, but not by a very large margin, Yao Jian, spokesman of China's

Ministry of Commerce, said on Tuesday. “To protect the environment and natural resources, China will stick to the

China's Ministry of quota system to manage rare earth exports next year, and quotas will also decline," Yao told Xinhua News Agency.

11-Nov-10 Though giving no clear extent of the decline, Yao's remarks echoed the comments of Wang Jian, a vice-minister of

Commerce

commerce, made on Monday at a news conference. "I believe China will see no large rise or fall in rare earth exports next

year," said Wang.

The EU trade chief said on Wednesday he would press China for assurances on rare earth supplies in talks next month,

though there was no conclusive evidence Chinese limits on such exports had hit European industry. The European

10-Nov-10 EU Trade Chief Union is struggling to secure supplies of rare earth minerals, which are used in the production of high-tech goods and

defense products, and has said it could take legal action against China for cutting down on exports.

"The Japanese and US foreign ministers have agreed that the two nations need to hold economic talks on issues

including rare earth minerals," Japan's Chief Cabinet Secretary Yoshito Sengoku told a news conference. "Of course the

Japan and the issue of how to diversify the procurement of rare earth minerals and other resources such as oil will be discussed with

9-Nov-10

United States the United States as well as with other countries," Sengoku said. Washington has called restrictions on the minerals a

potential threat to the US economy and national security.

A letter written by 37 groups including the US Chamber of Commerce, and various other business and trade

US Chamber of associations, urged G20 leaders to “refrain from export taxes, quotas or other market-distorting measures on rare-earth

8-Nov-10

Commerce elements that restrict global supply and unnecessarily contribute to price volatility,” reported an article by the AFP.

Trade Minister Chen Deming cautioned that other countries will have begun sharing the environmental burden of

Chinese Trade mining the metals in the future. “We are currently in talks with rare earth consuming countries and countries with rich

8-Nov-10 rare resources on how to produce rare earth in a more environmentally friendly way,” Chen said. “We also need to find

Minister

new rare earth resources.”

Mrs. Clinton, who is leaving Australia today after weekend defense and security talks, said the US and Australia "need

8-Nov-10 Hillary Clinton

to discuss in depth the supply of rare-earth minerals".

China's Ministry of China will maintain its export volume of rare earths next year, the official Xinhua News Agency said, citing Minister of

7-Nov-10

Commerce Commerce Chen Deming.

Chinese Industry China's industry ministry is considering regulations to tighten pollution standards for rare earth producers, Xinhua

7-Nov-10

Ministry news agency reported on Sunday, a move the country's top firm said might further raise export prices.

Chinese

The Chinese commerce minister Chen deming 5 in Paris dismissed some western media in China rare earth export

6-Nov-10 Commerce

untrue reports, and said China next year will remain rare earth exports.

minister

Source: Mackie Research Capital, Various news articles as listed

www.mackieresearch.com

17. Page 17

APPENDIX 1 (cont’d)

HIGHLIGHTS OF RARE EARTHS-RELATED NEWS

China will cut rare earth export quotas for 2011, but only by a small amount after slashing them this year, the

China's Ministry of Commerce Ministry said on Tuesday, calling the squeeze on exports a step to save the environment. “Given that

4-Nov-10 we've already had major reductions in export quotas over recent years, the extent of the fall in China's rare earth

Commerce

export volumes next year will not be great,” the brief Xinhua report cited him as saying.

China studying plan to build strategic reserves for ten minor metals, Shanghai Securities News reported last night,

3-Nov-10 Chinese Newspaper without citing anyone. Ten metals include rare earths.

The quota for rare earth exports could be reduced 3% to 10% in 2011 from this year’s levels after the 40% cut in

permitted exports in 2010, Matthew James, executive vice president for strategy at Australian miner Lynas Corp.,

3-Nov-10 Lynas Corporation recently told China Real Time. He said that as China restructures its rare earth industry domestically, there is less for

export. James predicted next year’s export quota on rare earths will emerge in two tranches, making it difficult to

know until mid-2011 exactly how much China will permit to leave.

China Securities Journal today quoted an unidentified source from China's Ministry of Commerce who said that the

country's rare metal export quota will be cut by 2 percent to 3 percent. "The export quotas for rare metals will

3-Nov-10 Chinese Newspaper unlikely rebound in the future," said an industry insider, who helped draft related policies, during an interview with

China Securities Journal.

China's Ministry of China will cut rare earth export quotas for 2011, but only by a small amount after slashing them this year, the

2-Nov-10 Commerce Ministry said on Tuesday, calling the squeeze on exports a step to save the environment.

Commerce

China ended its undeclared embargo of exports of crucial strategic minerals to the US, Europe and Japan, although

28-Oct-10 New York Times shipments to Japan still encountered difficulties, the New York Times reported, citing four unidentified rare earth

industry officials.

China has called off a meeting of its economics minister with his counterparts of Japan and South Korea, scheduled

27-Oct-10 Newspaper for the week-end, amidst a row over its policy of exporting rare earths, a Japanese media report said Wednesday.

China practices the quota license administration on the export of rare earth products since 1998. In recent

years, Chinese government cuts down the volume of export enterprises, export quotas and annual exploitation

volume of rare earth ores. China’s Ministry of Commerce declared that the total export quota of rare earth

25-Oct-10 Newspaper products of domestic-funded enterprises was 50,000 tons in 2005, 34,000 tons in 2008. In 2009, it set the total

export quota of 50,145.1 tons for domestic-funded and foreign-funded enterprises. In 2010, it cut down the

export quota to 30,258 tons, including 22,512 tons for domestic-funded enterprises and 7,746 tons for foreign-

funded enterprises.

A story has been published on the China Daily online website today stating that China will further reduce

19-Oct-10 Newspaper quotas for rare earth exports by 30 percent next year to protect the precious metals from over-exploitation.

Chinese premier Wen Jiabao in Brussels attended the 6th sino-european business summit, pointed out that

6-Oct-10 Chinese Premier “during a speech to the management and control of rare earth is necessary, but never blockade. China will not

put rare earth as a bargaining tool; our purpose is to the sustainable development of the world.”

China, the world’s largest rare- earths producer, cut export quotas for the minerals needed to make hybrid cars

9-Jul-10 Bloomberg and televisions by 72 percent for the second half. Shipments will be capped at 7,976 metric tons, down from

28,417 tons for the same period a year ago, according to data from the Ministry of Commerce yesterday.

In 1985, China began to implement the export tax rebate policy for rare earth products. From January 1, 2004,

export tax rebate for rare earth metals was adjusted from 13% to zero, the export tax rebate rate for yttrium

metal, scandium metal and its compounds, inorganic or organic compounds was adjusted from 17%, 13% to

7-Apr-10 Article 5%. From May 1, 2005, the export tax rebates for rare earth metals, rare earth oxides, rare earth salts were

abolished. On November 1, 2006, the regulation of imposing export tariffs on rare earth products was released

and would implement by June 1, 2007, the tax rate was 10%.

Chinese export quotas have been decreasing each year for the last 8 years. Most recently, China has announced

8-Jul-09 Newspaper that export quotas for the first half of 2009 are being reduced by approximately 34% over the same period last

year.

Source: Mackie Research Capital, Various news articles as listed

www.mackieresearch.com

18. Page 18

APPENDIX 2

Source: US Department of Energy, Mackie Research Capital, IMCOA; Price Forecast Source: Mackie Research Capital

www.mackieresearch.com

19. Page 19

Source: US Department of Energy, Mackie Research Capital, IMCOA; Price Forecast Source: Mackie Research Capital

www.mackieresearch.com

20. Page 20

Source: US Department of Energy, Mackie Research Capital, IMCOA; Price Forecast Source: Mackie Research Capital

www.mackieresearch.com

21. Page 21

Source:

US Department of Energy, Mackie Research Capital, IMCOA; Price Forecast Source: Mackie Research Capital

www.mackieresearch.com

22. Page 22

Source: US Department of Energy, Mackie Research Capital, IMCOA; Price Forecast Source: Mackie Research Capital

www.mackieresearch.com

23. Page 23

Source: US Department of Energy, Mackie Research Capital, IMCOA; Price Forecast Source: Mackie Research Capital

www.mackieresearch.com

26. Page 26

RELEVANT DISCLOSURES

1. N/A

ANALYST CERTIFICATION

Each analyst of Mackie Research Capital Corporation whose name appears in this report hereby certifies that (i) the recommendations and

opinions expressed in this research report accurately reflect the analyst’s personal views and (ii) no part of the research analyst’s

compensation was or will be directly or indirectly related to the specific conclusions or recommendations expressed in this research report.

I n f o r ma t i o n a b o u t M a c k i e R e s e a r c h C a p i t a l C o r p o r a t i o n ’ s R a t i n g S y s t e m, t h e d i s t r i b u t i o n o f o u r r e s e a r c h t o c l i e n t s a n d t h e p e r c e n t a g e o f r e c o m me n d a t i o n s wh i c h a r e i n

e a c h o f o u r r a t i n g c a t e g o r i e s i s a v a i l a b l e o n o u r we b s i t e a t ww w. ma c k i e r e s e a r c h . c o m.

The information contained in this report has been drawn from sources believed to be reliable but its accuracy or completeness is not guaranteed, nor in providing it does Mackie Research Capital

Corporation assume any responsibility or liability. Mackie Research Capital Corporation, its directors, officers and other employees may, from time to time, have positions in the securities

mentioned herein. Contents of this report cannot be reproduced in whole or in part without the expressed permission of Mackie Research Capital Corporation. (U.S. Institutional Clients — Research

Capital U.S.A. Inc. (a wholly owned subsidiary of Mackie Research Capital Corporation) accepts responsibility for the contents of this report subject to the terms & limitations set out above. Firms

or institutions receiving this report should effect transactions in securities discussed in the report through Research Capital U.S.A. Inc., a Broker-Dealer Registered with the United States Securities

and Exchange Commission).

Toronto 416.860.7600 Montreal 514.399.1500 Vancouver 604.662.1800 Calgary 403.218.6375 Regina 306.566.7550 St. Albert 780.460.6460

www.mackieresearch.com