Highlights on Global Central Bank Policy Rates as on July 2014

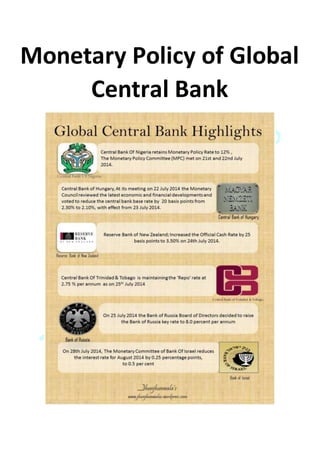

Highlights on Global Central Bank Policy Rates as on July 2014 #CentralBankOfHungary reduced BaseRate by 20 basis points to 2.10% with effect from 23rd July 2014 #Hungary #MagyarNemztiBank #MNB #CentralBankOfRussia raised #KeyRate to 8.0 % on July 25th 2014 , #Russia #CBR #BankOfRussia #ReserveBankOfNewZealand raised OfficialCashRate by 25 basis points to 3.50% on 24th July 2014 , #RBNZ #NewZealand #CentralBankofNigeria retains #MonetaryPolicyRate at 12% #MPR,#MPC Monetary Policy Comittee met on 21st and 22nd July 2014. #MonetaryPolicy of #CentralBankofTrinidadAndTobago maintains #RepoRate at 2.75% #BankOfIsrael , As on 28th July 2014 the #MonetaryCommittee reduces the #InterestRate for August 2014 by 0.25 percentage points, to 0.5 percent, #BankIsrael #CentralBankOfIsrael #Israel

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (13)

Similar to Highlights on Global Central Bank Policy Rates as on July 2014

Similar to Highlights on Global Central Bank Policy Rates as on July 2014 (20)

More from Jhunjhunwalas

More from Jhunjhunwalas (20)

Recently uploaded

Recently uploaded (20)

Highlights on Global Central Bank Policy Rates as on July 2014

- 1. Monetary Policy of Global Central Bank

- 5. PRESS RELEASE ON THE MONETARY COUNCIL MEETING OF 22 JULY 2014 ( CENTRAL BANK OF HUNGARY ) At its meeting on 22 July 2014, the Monetary Council reviewed the latest economic and financial developments and voted to reduce the central bank base rate by 20 basis points from 2.30% to 2.10%, with effect from 23 July 2014. In the Council’s judgement, Hungarian economic growth is likely to continue. While the pace of economic activity is strengthening, output remains below potential and is likely to approach that level in the course of next year. Despite the pick-up in domestic demand, capacity utilisation is expected to improve only gradually due to the protracted recovery in Hungary’s export markets. With employment rising, the unemployment rate is falling, but still exceeds its long-term level determined by structural factors. Inflationary pressures in the economy are likely to remain moderate for an extended period. Based on the inflation data for June, consumer prices continue to show historically low dynamics. The Bank’s measures of underlying inflation capturing the medium-term outlook still indicate moderate inflationary pressures in the economy, reflecting low inflation in external markets, the degree of unused capacity in the economy, subdued wage dynamics, the fall in inflation expectations and the reductions in administered prices, implemented in a series of steps. Domestic real economic and labour market factors continue to have a disinflationary impact and low inflation is likely to persist for a sustained period. However, domestic demand-side disinflationary pressures are weakening gradually as activity gathers pace, and inflation is likely to reach levels around 3 per cent consistent with price stability at the end of the forecast horizon. Based on data available since the latest interest rate decision, economic growth continued, as reflected in data for industrial production and retail trade. In the Council’s judgement, the Hungarian economy returned to a growth path in 2013. Looking ahead, economic growth may continue in a more balanced pattern than previously, with the recovery in domestic demand likely to make a greater contribution. Investment is likely to continue accelerating, reflecting the increasing use of EU funding and the easing in credit constraints also due to the Bank’s Funding for Growth Scheme. Household consumption is also likely to grow gradually, mainly as a result of the expected increase in the real value of disposable income and the reduced need for deleveraging. However, propensity to save is expected to remain above levels seen prior to the crisis. Based on labour market data for May, the number of employees, excluding those employed under public employment programmes, remained broadly unchanged relative to the previous month, and the unemployment rate fell. The labour market is expected to become tighter. International investor sentiment was volatile in the past month, mainly reflecting the escalation of geopolitical conflicts and weaker-than-expected European macroeconomic data. Hungarian risk premia remained broadly unchanged in the period and the forint exchange rate depreciated slightly, with country-specific factors playing a role, in addition to external factors. Hungary’s persistently high external financing capacity

- 6. and the resulting decline in external debt have contributed to the reduction in its vulnerability. The announcement of the Bank’s self-financing concept may contribute to an improvement in perceptions of the risks associated with the domestic economy. In the Council’s judgement, a cautious approach to policy is warranted due to uncertainty about future developments in the global financial environment. In the Council’s judgement, there remains a degree of unused capacity in the economy and inflationary pressures are likely to remain moderate for an extended period. The negative output gap is expected to close gradually at the monet ary policy horizon. In the Council’s judgement, it was justified to end the easing cycle because of the need to remove uncertainty about the bottom of the interest rate path, and the medium-term achievement of price stability made it necessary to implement a further 20 basis point reduction in interest rates. The Council judges that the central bank base rate has reached a level which ensures the medium-term achievement of price stability and a corresponding degree of support for the economy. That means that the two-year easing cycle of a significant cumulative reduction of 490 basis points has ended. Looking ahead, the macroeconomic outlook points in the direction of persistently loose monetary conditions. The abridged minutes of today’s Council meeting will be published at 2 p.m. on 6 August 2014. Magyar Nemzeti Bank Monetary Council

- 7. The Central Bank of the Russian Federation (Bank of Russia) On Bank of Russia key rate On 25 July 2014 the Bank of Russia Board of Directors decided to raise the the Bank of Russia key rate to 8.0 percent per annum. Inflation deceleration in July 2014 has been slower than expected. At the same time, inflation risks have increased due to a combination of factors, including, inter alia, the aggravation of geopolitical tension and its potential impact on the ruble exchange rate dynamics, as well as potential changes in tax and tariff policy. The build-up of these risks will lead to inflation expectations remaining heightened and creates threats of inflation exceeding the target in the coming years. The adopted decision is aimed at slowing the consumer price growth to the 4.0% target level in the medium term. If high inflation risks persist, the Bank of Russia will continue raising the key rate. In June 2014, the year-on-year consumer price growth rate increased to 7.8% and core inflation grew to 7.5%. Meanwhile, inflation expectations stayed elevated. The main reason for inflation acceleration was the effect of the observed ruble depreciation on prices of a wide range of goods and services. Moreover, there were a number of specific factors boosting prices for some food items. July has seen signs of inflation slowdown. However, deceleration in consumer price growth has been slower than expected. The annual consumer price growth rate stood at estimated 7.5% as of 21 July. Inflation deceleration was mainly caused by lower increases in administered prices and utility tariffs. Price growth rates for other goods and services have stabilised as a result of decreasing impact of ruble depreciation seen in January-March 2014 on consumer prices, along with improved conditions in food markets due to, inter alia, the new harvest coming in. Monetary conditions have been tightening since March 2014, inter alia due to geopolitical factors. Interest rates on bank loans and ruble deposits increased. Lending growth slowed down slightly following the acceleration in the previous months. The year- on-year money supply growth rate has decreased which sets conditions for a decline in inflation in the medium term. Over Q2 2014 the moderate recovery of economic activity has been observed. According to the Bank of Russia estimates, the GDP growth rate was close to zero in Q2 following negative figures earlier. Low economic growth rates are largely caused by structural factors. Utilisation of production factors — labor force and commercially viable production capacities — is high. Labour productivity growth is sluggish. Due to the demographic trends labour force shortage will continue to affect economic growth in the long term. Along with structural factors, external political uncertainty has a negative impact on economic activity. Investment demand remains weak amid low business confidence, limited access to long-term financing in both international and domestic markets, and declining profits in the real sector. Besides, consumer activity is cooling. Economic slack in most countries that are Russia’s trading partners does not contribute to acceleration in economic growth. At the same time, persistently high oil prices support domestic economy.

- 8. Under the scenario of no negative shocks, annual inflation will decline in the second half of 2014. The factors of inflation decline are exhausted impact of ruble depreciation seen in January-March 2014 on consumer prices, lower scale of increase in administered prices and tariffs, expected good harvest, as well as subdued aggregate demand with aggregate output of goods and services remaining below potential. At the same time, there is an increased probability of negative trends which may result in inflation acceleration. These shocks include aggravation of geopolitical tension, adjustments in monetary policy of foreign central banks and the potential impact of those factors on national currency exchange rate dynamics, t ax and tariff policy changes under discussion. Against this background the adopted decision will set conditions for a decline in annual consumer price growth rates to 6.0-6.5% by the end of 2014 and to the target level of 4.0% in the medium term. If high inflation risks persist, the Bank of Russia will continue raising the key rate. The next meeting of the Bank of Russia Board of Directors on the key rate is scheduled for 12 September 2014. The press-release on the Bank of Russia Board of Directors’ decision is to be published at 13:30 Moscow time.

- 9. Reserve Bank Of New Zealand raises OCR to 3.5 percent Statement issued by Reserve Bank Governor Graeme Wheeler: The Reserve Bank today increased the Official Cash Rate (OCR) by 25 basis points to 3.5 percent. New Zealand’s economy is expected to grow at an annual pace of 3.7 percent over 2014. Global financial conditions remain very accommodative and are reflected in low interest rates, narrow risk spreads, and low financial market volatility. Economic growth among New Zealand’s trading partners has eased slightly in the first half of 2014, but this appears to be due to temporary factors. Construction, particularly in Canterbury, is growing strongly. At the same time, strong net immigration is adding to housing and household demand, although house price inflation has moderated further since the June St atement. Over recent months, export prices for dairy and timber have fallen, and these will reduce primary sector incomes over the coming year. With the exchange rate yet to adjust to weakening commodity prices, the level of the New Zealand dollar is unjustified and unsustainable and there is potential for a significant fall. Inflation remains moderate, but strong growth in output has been absorbing spare capacity. This is expected to add to non-tradables inflation. Wage inflation is subdued, reflecting recent low inflation outcomes, increased labour force participation, and strong net immigration. It is important that inflation expectations remain contained. Today’s move will help keep future average inflation near the 2 percent target mid-point and ensure that the economic expansion can be sustained. Encouragingly, the economy appears to be adjusting to the monetary policy tightening that has taken place since the st art of the year. It is prudent that there now be a period of assessment before interest rates adjust further towards a more-neutral level. The speed and extent to which the OCR will need to rise will depend on the assessment of the impact of the tightening in monetary policy to date, and the implications of future economic and financial data for inflationary pressures.

- 10. Central Bank of NigeriaCommuniqué No. 96 of the Monetary Policy Committee Meeting,July 21-22,2014 The Monetary Policy Committee (MPC) met on July 21 and 22, 2014 against the backdrop of continuing QE3 tapering by the U.S Federal Reserve which has resulted in the slowing of inflows to emerging markets and frontier economies; and the attendant uncertainties in the outlook for monetary policy and financial stability in the post-tapering period. The meeting was attended by 10 members. A new member, Prof. Dahiru Hassan Balami, whose appointment had recently been confirmed by the Senate, was also in attendance. The Committee deliberated on key external and domestic economic developments and considered the Banking Stability Report since the 2 MPC meeting of May 2014 as well as the outlook for the rest of the year. The global monetary policy environment appears to be further complicated by risks posed by continued currency crisis and fragility in Europe, geo-political tensions in the Middle East and a number of emerging and developing economies. Domestically, the policy challenges remain. These include the uptick in inflation, anticipated increased spending towards the general elections and the possible effects of US tapering on the domestic market. International Economic Developments The Committee noted that the rebound in global economic activity strengthened in the first half of 2014; although at levels lower than previously projected. The tapered growth arose mainly from the emerging and developing economies owing to the rising real interest rates and geo-political crisis. On the whole, the effects of the global financial crisis have continued to wane even as the issues of rising income inequality, unemployment and poverty appear to be 3 gaining prominence; engaging the attention of the monetary authorities. These latest projections indicate that the euro area is gradually coming out of recession, as growth projection for 2014 is positive for all member countries albeit with significant variation. Growth is expected to be stronger in the core EU countries while high debt and financial fragmentation continue to weigh on aggregate domestic demand in the peripheral countries. For the entire euro zone, there is a risk of low inflation or outright deflation which could result in higher real interest rates that may constrain output expansion. In the emerging and developing economies, growth is projected at 5.0 per cent in 2014 from 4.7 per cent in 2013, buoyed by stronger external demand from the advanced countries. The key downside risks in the developing and emerging economies include: political uncertainty, exchange rate realignment in response to changing fundamentals, further monetary tightening to address emerging currency crisis, and tighter external financing conditions arising from the rapid normalization of the US monetary policy. Inflation is 4 projected to remain subdued in 2014 and 2015, partly reflecting the significant output gaps in the developed economies, weaker domestic demand in developing and emerging economies, and sliding commodity prices, especially fuels and food. In the advanced economies, inflation is currently below target and its return to the long run

- 11. trend could take a while due to the slow pace of economic recovery. Likely depreciation in currencies, domestic demand pressure, and capacity constraints could pose upside risks to inflation in the emerging market economies. The Committee noted that the stance of monetary policy could diverge across regions over the medium term on account of variations in risks and ot her challenges confronting various economies. The US is expected to commence tightening by the second half of 2015 as inflation hits the long run target and unemployment rate falls to the threshold level. The euro area and Japan are expected to continue with supportive monetary policy due to low inflation including threat of deflation in some countries, 5 weak recovery, weakness in bank balance sheets, and strong demand for their bonds as a result of low sovereign risk. Majority of the central banks remained cautious with regard to the stance of monetary policy. While most advanced economies are likely to maintain an accommodative stance for monetary policy for the rest of the year to firm up aggregate demand and employment, the major impetus for monetary policy adjustments in the emerging markets and developing economies could come from the effects of the US Fed’s tapering of QE3 on their currencies and the financial markets. Domestic Economic and Financial Developments Output The National Bureau of Statistics (NBS) reported revised growth numbers from 2010 to 2013 and the first quarter of 2014, as part of the GDP rebasing exercise. Accordingly, the estimated growth rate for 2013 now stands at 5.49 per cent, compared with 5.31 and 4.21 per cent recorded in 2011 and 2012, respectively. Similarly, the 6 revised estimate of 6.77 per cent for the fourth quarter of 2013 was an improvement over the 5.17 and 3.64 per cent in the previous quarter and the corresponding period of 2012, respectively. In the first quarter of 2014, real GDP growth was 6.21 per cent, which was higher than the corresponding quarter of 2013. In line with the trend, the non-oil sector was the main driver of growth in the first quarter of 2014, recording 8.21 per cent growth. The key growth drivers in the non-oil sector in the first quarter of 2014 remained industry, agriculture, trade, and services which contributed 1.77, 1.26, 1.26 and 3.15 per cent, respectively. The oil sector continued to record improvements in performance with its growth rate improving from -9.36 and -11.40 per cent, respectively, in the fourth and first quarters of 2013, to -6.60 per cent in the first quarter of 2014. The Committee welcomed the impressive growth performance but noted that the country has the potential to do better with appropriate supportive macroeconomic policies. The Committee, therefore, stressed the imperatives for monetary policy to sustain efforts aimed at supporting non-inflationary growth in key sectors of 7 the economy. The Committee also emphasized the need for government to sustain and deepen tax revenue and enhance efforts aimed at fast-tracking the structural transformation of the economy with a view to making it resilient to adverse shocks as well as creating the necessary platforms for reducing unemployment, income inequality, and poverty in the country. Prices

- 12. Developments in the aggregate price level suggest an underlying inflationary pressure since January 2014. The year-on-year headline inflation steadily inched up marginally from 7.9 per cent in April to 8.0 per cent in May 2014 and further to 8.2 per cent in June. The up- tick in June was, however, largely attributed to the rise in food inflation which rose from 9.7 per cent in May 2014 to 9.8 per cent in June while core inflation, on the other hand, rose from 7.7 per cent in May 2014 to 8.1 per cent in June. The Committee noted that all measures of inflation have witnessed progressive upward trend since February 2014 and agreed that this trend should be monitored closely to achieve a reversal. 8 Monetary, Credit and Financial Markets’ Developments Broad money (M2) rose by 1.66 per cent in June 2014 over the level at end-December 2013, indicating an annualized growth rate of 3.31 per cent. The annualized growth rate was considerably lower than the growth benchmark of 15.52 per cent for fiscal 2014. For the same period, net domestic credit increased by 0.88 per cent compared with the growth rate of 15.39 per cent over the corresponding period of 2013. When annualized, net domestic credit rose by 1.77 per cent, compared with the growth benchmark of 28.5 per cent for fiscal 2014. The expansion in aggregate domestic credit was mainly due to the increase in claims on the private sector which increased by 2.75 per cent in June 2014, which was however, moderated by the contraction in net credit to Government. Meanwhile, money market rates remained within the MPR corridor during the review period. The monthly weighted average OBB rate was 10.38 per cent in May 2014 but it increased by 14 basis points to 9 10.52 per cent in June. The uncollaterized overnight rate was 10.50 per cent in June 2014, compared with 10.63 per cent in May 2014. Overall, both the OBB and overnight call rates were trading closer to the lower bound of the MPR corridor on account of liquidity surfeit in the banking system. Activities in the capital market were bullish during the period with the All-Share Index (ASI)increasing by 2.8 per cent from 41,329.19 at end-December 2013 to 42,482.48 at end-June 2014. Market capitalization also moved in the same direction. External Sector Developments All the segments of the foreign exchange market witnessed a considerable degree of stability during the period. The exchange rate at the retail-Dutch Auction System Segment (rDAS)of the market was flat at N157.29/US$ in the review period. At the inter-bank market, the selling rate opened at N162.20/US$ and closed at N162.95, representing a depreciation of N0.75 or 0.46 per cent. Conversely, at the BDC segment, the exchange rate opened at N167.00/US$ and closed at N168.00/US$, representing a depreciation of N1.00 or 0.6 per cent. 10 Gross official reserves rose to US$40.20 billion by 18 July from US$37.31 billion at end-June 2014. The increase in reserves was mainly due to increased accretion and moderation in the rate of depletion. The Committee’s Consideration The Committee was satisfied with the relative stability in the macroeconomy as reflected in the impressive growth rates, stable consumer prices and exchange rate as well as increased external reserves. It was however concerned about the weak translation of stability to microeconomic gains in employment and access to finance especially by

- 13. small and medium scale businesses. It, therefore, emphasized the need for the MPC decisions to take into account the long run impact on employment level, wealth creation and growth of businesses. The Committee noted the potential of the power sector to stimulate output growth through enhanced investment and the spill-over effect in employment generation if the challenges confronting the sector are effectively and appropriately addressed. Specifically, it 11 noted that gas-to-power has remained a binding constraint in reaping the benefits of the recently-concluded power sector reforms; urging for the collective efforts of government, private investors and the banks to resolve. Other pressure points include the underlying pressure from food/core inflation and the risks that could emanate from the likely increase in aggregate spending in the run up to the 2015 general elections. The Committee was also concerned about the implications of the on-going QE3 tapering for inflows and external reserves. The Committee recognized the necessity of sustaining a stable naira exchange even as it has to deal with the delicate balancing of the need for a low interest rate regime. The Committee noted that portfolio flows were not employment generating but were essential in the absence of adequate fiscal buffers. The Committee welcomed the moderation in the rate of depletion in external reserves in recent months, noting that reserves accretion needed to improve much faster to provide a strong and more resilient buffer to fiscal operations. The Committee, however, noted 12 that a gradual reduction in the country’s import bills through domestic production of some of the major food imports should be a key element in the overall reserves accretion strategy. It welcomed the decision of the Bank to collaborate with other stakeholders in this regard. The Committee further expressed concern about the liquidity level and the trending uptick in inflation which may not be unconnected with the poor harvest in some agricultural producing areas, particularly in the north eastern and central states of the country. It however, noted that other reform measures could dampen food prices in the short to medium term and restore inflation to a sustainable long-run path. Overall, the Committee noted that the policy direction of inflation, exchange rate and interest rate must be seen not only in the context of price and financial stability but also in enhancing the quality of life of Nigerians and promoting employment generation. 13 The Committee’s Decisions In view of these developments, the Committee decided by a unanimous vote to retain the current stance of monetary policy with one member voting for an asymmetric corridor around the MPR. Consequently, the MPC voted to: (i) Retain the MPR at 12 per cent with a corridor of +/- 200 basis points around the midpoint; (ii) Retain the Liquidity Ratio at 30 per cent; (iii) Retain the public sector Cash Reserve Requirement at 75.0 per cent; and (iv)Retain the private sector Cash Reserve Requirement at 15.0 per cent.

- 14. CENTRAL BANK OF TRINIDAD & TOBAGO MONETARY POLICY ANNOUNCEMENT (July 25, 2014 ) CORE INFLATION REMAINS STABLE; CENTRAL BANK MAINTAINS REPO RATE AT 2.75 PER CENT. With core inflationary pressures well contained, the Central Bank is maintaining the ‘Repo’ rate at 2.75 per cent which remains supportive of current economic conditions. However, as the pace of economic activity strengthens, the Central Bank is giving greater consideration to managing inflationary expectations in calibrating its monetary policy instruments. As of late July 2014, signals are mixed regarding the outlook for global growth. In its latest World Economic Outlook (WEO) Update, the IMF indicates that the global recovery continues but at an uneven pace, and that downside risks remain. In the United States, earlier optimism about growth prospects has moderated following an unanticipated sharp contraction in the first quarter of 2014, even though a rebound in activity is already underway. Growth is improving for some economies in the Euro zone, while the economic recovery in the United Kingdom appears to be sustainable. Growth in most emerging markets, including China, remains at a slower pace than before, partly due to softer external demand. Although geopolitical tensions are escalating in several regions around the world, expectations of changes in monetary policy in the major industrial economies dominate sentiment in global financial markets. The United Kingdom is expected to be the first advanced economy to raise interest rates, albeit at a moderate pace, while the US Federal Reserve is not anticipated to raise interest rates until later in 2015. By contrast, the European Central Bank (ECB) recently announced a package of policy measures to stimulate bank lending and to address the risk of a prolonged period of low inflation in the Euro area. At home, the corporate sector is still cautiously optimistic in its outlook for business activity and economic strength. Results from the Central Bank’s second Business Confidence Survey, conducted in the second quarter of 2014 in conjunction with the Arthur Lok Jack Graduate School of Business, showed that almost 80 per cent of firms expect to increase their production levels over the next six months. More firms were also confident that the local economy would improve over the next 12 months than in the first survey. On the other hand, 66 per cent of all businesses expect their financial position to improve in the next 12 months, down from 75 per cent of firms in the first quarter of 2014. A recovery in business lending and steady growth in consumer loans provide support to the positive business sentiment. On a year-on-year basis, private sector credit granted by the consolidated financial system expanded by more than 6 ½ per cent in May 2014 – the fastest rate since February 2009. Business lending grew for the fourth consecutive month, also, by around 6 ½ per cent in May 2014, from just over 3 ½ per cent in April 2014. Consumer lending remained robust, growing at around 7 ½ per cent in May 2014. Meanwhile, the pace of real estate mortgage loans slowed to just over 10.0 per cent in May 2014 from 14 ½ per cent at the start of the year. Core inflation remained relatively stable in the first half of 2014. On a year-on-year basis, core inflation stood at 2 ½ per cent by the end of June 2014. Headline inflation slowed to

- 15. 3.0 per cent while food inflation eased for the third consecutive month to 3 ½ per cent in June 2014. Rising consumer demand, higher Government spending and second round effects from the recent increase in cement prices could help to accelerate inflationary pressure later in the year. Excess liquidity in the banking system fell below $5 billion in the first three weeks of July 2014. Commercial banks’ excess reserves dropped to a daily average of around $5.0 billion over the period July 1 – 21, 2014 from a little over $7.5 billion in June and close to $8.5 billion in May 2014. In June 2014, the Central Bank issued a seven-year, 2.2 per cent coupon, liquidity sterilization Treasury bond, which removed approximately $1.0 billion from the financial system. In addition, Central Government’s operations, which are usually the main source of banking system liquidity, resulted in a net domestic withdrawal of roughly $1.3 billion in the first three weeks of July 2014. Further, Central Bank’s support to the foreign exchange market in July also indirectly withdrew $1.1 billion from the system. Interest rate differentials between TT and US Treasury securities, though still low, have stabilized in positive territory over the past few months, particularly at shorter tenors. The three-month domestic Treasury Bill rate increased marginally to 0.13 per cent in mid-July 2014 from 0.12 per cent at the end of June 2014. With the three-month US Treasury Bill rate holding at 0.03 per cent, the TT-US interest differential widened slightly to 10 basis points as at July 21, 2014 from 9 basis points at the end of June 2014. Meanwhile, despite the on- going reduction in the US Federal Reserve’s quantitative easing programme, strong external demand has placed some downward pressure on longer term US Treasury yields in recent months. As such, the interest rate differential between TT and US 10-year Treasury yields remained in positive territory at around 14 basis points as at July 21, 2014 from 10 basis points at the end of June 2014. The Central Bank will continue to closely monitor economic conditions and is prepared to take further action, if necessary. The next Monetary Policy Announcement is scheduled for September 26, 2014.

- 16. Central Bank Of Israel The Monetary Committee reduces the interest rate for August 2014 by 0.25 percentage points, to 0.5 percent Inflation data: The Consumer Price Index (CPI) for June increased by 0.3 percent , slightly above forecasters’ projections for an increase of 0.2 percent, on average. There was a relatively large seasonal increase in the clothing and footwear component, and a marked decline in the fruit and vegetables component. The inflation rate over the preceding 12 months was 0.5 percent, and the CPI excluding the housing component declined by 0.2 percent over that period. The tradable goods components of the CPI declined by 1.2 percent over the past 12 months. The rate of increase in components consisting of nontradable products also moderated, and they increased by only 1.4 percent. Inflation and interest rate forecasts: A gradual but continued decline can be seen in inflation expectations derived from various sources since the April CPI was published. Private forecasters’ projections for the next 12 CPI readings declined slightly this month, to 1.3 percent on average. Inflation expectations for the coming year derived from the capital market declined to 1.2 percent (seasonally adjusted), and two-year projections declined to 1.5 percent. (In the recent period there has been a difficulty in calculating 1- year expectations because there aren’t CPI-indexed bond series for that range.) Expectations for the next 12 CPI readings derived from banks’ internal interest rates declined to 1 percent. Inflation expectations for medium and long terms were virtually unchanged this month, after they declined markedly since the April CPI was published, and expectations for medium terms remained below the midpoint of the inflation target range. Most forecasters are of the opinion that the interest rate will not be reduced in the coming quarter. The makam and Telbor curves indicate some probability of one interest rate reduction in the coming three months. Real economic activity: Data on real economic activity which became available this month refer to the period before the beginning of Operation Protective Edge, and they indicate that the economy continues to grow at a moderate rate, similar to that of previous quarters. It is still too early to tell the economic effects of the security situation, but the effect of security events of similar magnitude in the past decade turned out to be a moderate macroeconomic impact, up to about 0.5 percent of GDP (in the Second Lebanon War). The recovery from previous events was generally rapid, but the negative impact on some industries, particularly the tourism industry, is liable to last longer. The Composite State of the Economy Index increased by 0.1 percent in June—its growth rate

- 17. was moderated by the trade and services revenue indices and by goods exports. Against the background of an absence of growth in world trade, goods exports (excluding ships and automobiles and diamonds, in dollar terms) declined by 9 percent in the second quarter, after an increase of 3 percent in the first quarter. This was the result of moderation in high technology and medium-high technology exports, led by declines in exports of pharmaceuticals and chemicals. Goods imports (excluding ships and aircraft, diamonds, and fuels, in dollar terms) remained virtually unchanged in the second quarter. Services exports continued to grow, and they increased by 0.7 percent in April–May compared with the first quarter. Revenue from trade and services industries continued to moderate, declining by 1.3 percent in April–May compared with the first quarter. The various indices of expectations this month are based on surveys conducted before Operation Protective Edge began. Consumer confidence indices for June were mixed—those compiled by the Central Bureau of Statistics and Bank Hapoalim declined, after increasing in recent months, while the Globes index was stable. The Purchasing Managers Index declined sharply and returned to the range indicating contraction of activit y. The labor market: Labor Force Survey data in recent months have indicated stability; among the principal working ages (25–64), in May, the participation rate was 79.6 percent and the employment rate was 75.5 percent, and in April–May they remained virtually unchanged compared with the first quarter. The unemployment rate in May for that age range was 5.2 percent, and its average level over April–May increased slightly after declining in the first quarter. The overall unemployment rate was 5.9 percent in May. The number of employee posts did not increase in February–April compared with the preceding three months (seasonally adjusted data), the result of a 0.4 percent decline in the number of employee posts in the business sector in contrast with an increase of 0.6 percent in the number of employee posts in public services. The job vacancy rate increased by 4 percent in the second quarter compared to the first quarter. Nominal and real wages increased by 0.6 percent in February–April, compared to the preceding three months (November–January, seasonally adjusted data). Health tax receipts, which provide an indication of total wage payments in the economy, were 5.3 percent higher in May–June, on a nominal basis, than in the corresponding two months of the previous year. Budget data: Since the beginning of 2014, the deficit in the government’s domestic activity (excluding net credit) was about NIS 2.3 billion, which is about NIS 4.5 billion smaller than the deficit in the seasonal path consistent with meeting the deficit target for 2014, because the level of expenditure is below the seasonal path consistent with full performance of the budget—domestic expenditures (excluding credit) in January–June were about NIS 5.8 billion lower than the path. Tax revenues in June were similar, in real terms, to those in June last year (excluding legislative changes and one-time revenues, and excluding extraordinary activities). Gross domestic VAT receipts, net of legislative changes, one-time revenues, and extraordinary activities were 0.4 percent lower in real

- 18. terms in June than in the corresponding month of last year. It is still too early to assess the effects of Operation Protective Edge on the budget, in terms of both direct defense expenditures and the cost of compensation and lost tax revenues. The foreign exchange market: From the monetary policy discussion on June 22, 2014, through July 25, 2014, the shekel strengthened by 0.5 percent against the dollar and by 1.5 percent against the euro. In terms of the nominal effective exchange rate, the shekel strengthened by about 0.8 percent this month. For the year to date, the effective exchange rate has strengthened by about 2 percent. On global markets the dollar traded mixed this month. The capital and money markets: No notable effect of the security situation was felt on financial markets. From the monetary policy discussion on June 22, 2014, through July 25, 2014, the Tel Aviv 25 Index declined by 0.5 percent, similar to the global trend. In the government bond market, the yield curve of CPI-indexed bonds flattened this month, and the unindexed-bond yield curve declined by up to 10 basis points. The yield on 10-year unindexed bonds declined by about 8 basis points, to 2.76 percent. The yield differential between 10-year Israeli government bonds and corresponding 10-year US Treasury securities widened slightly, to 30 basis points, but still remains at a low level compared with recent years. Makam yields increased slightly along the entire curve, and the 1-year yield is 0.64 percent. Israel's sovereign risk premium as measured by the five-year CDS spread increased by about 12 basis points, to 90 basis points, after a prolonged decline over the past year. The money supply: In the twelve months ending in June, the M1 monetary aggregate (cash held by the public and demand deposits) increased by 17.3 percent, and the M2 aggregate (M1 plus unindexed deposits of up to one year) increased by 7.7 percent. The credit markets: Total outstanding debt of the business sector increased by about NIS 5.5 billion (0.7 percent) in May, to NIS 786 billion, primarily as a result of net (nonbank) debt raised. In the past two months, a halt can be seen in the trend of decline in business sector debt. In June, the nonfinancial business sector issued bonds totaling about NIS 3.6 billion, compared with a monthly average of NIS 3.1 billion over the past year. Corporate bond market spreads increased since June, and for the first time since 2012 there was a monthly negative net new investment in corporate bond mutual funds. However, it is too early to determine if this is a change in trend. Outstanding household debt increased by about NIS 3.2 billion (0.8 percent) in May, to about NIS 417 billion. Half of that increase derives from housing debt. In June, new mortgages taken out totaled about NIS 4.6 billion, so that monthly new mortgage volume remained at its elevated level. There was an

- 19. additional slight decline in risk characteristics of new mortgages due to the steps taken by the Supervisor of Banks. In June, the interest rate on new mortgages taken out declined for all indexation tracks—the average interest rate on new CPI-indexed loans declined by about 0.07 percentage points, and the interest rate on new unindexed loans declined by about 0.02 percentage points. The housing market: The housing component of the CPI (based on residential rents) increased by 0.3 percent in June. In the 12 months ending in June, this component increased by 2.3 percent, a similar rate to that of the previous two months. Home prices, which are measured in the Central Bureau of Statistics survey of home prices but are not included in the CPI, increased by 0.5 percent in April–May. Over the 12 months ending in May, home prices increased by 8.8 percent, compared with an increase of 8 percent in the 12 months ended in April. In the 12 months ended in April, there were 45,800 building starts and 41,900 building completions. The number of new homes built through private initiative that remain for sale increased by 5 percent in April–May compared to the first quarter, reaching a historically high level. In April, the number of transactions declined by 25 percent compared to March, and preliminary indications are that this low level was maintained in May as well. The global economy: The IMF again revised its 2014 global growth and global trade forecasts downward—by 0.3 percent. The forecast was reduced for both advanced and developing economies. In contrast, the forecast for 2015 remained unchanged. In May, the first quarter’s trend of contraction in world trade continued. Assessments regarding the US are that the negative growth in the first quarter will not affect the GDP growth rate during the rest of the year, which will total 3 percent, so that growth for the full year of 2014 will be about 1.7 percent. The recent positive trend in business activity in the US continues, and is reflected both in data on economic activity and in activity surveys. In the labor market, total nonfarm payroll employment increased by a greater-than- expected 288,000 in June, and the unemployment rate declined to 6.1 percent. With that, salaries are increasing at a moderate pace, and assessments are that the low unemployment rate derives from the fact that many unemployed individuals have stopped looking for work. There are also indications of improvement in personal consumption expenditure and in consumer confidence. Inflation remains below 2 percent, and assessments are that the tapering process will continue as planned, and that the interest rate will only begin to be increased in the middle of 2015. This month, the Federal Reserve Chair emphasized that the interest rate tool is primarily intended to support inflation and employment targets, and less so to support financial stability. Weakness continues in Europe’s economy: Manufacturing data were disappointing, the recovery in the employment market is very moderate, and the unemployment rate remains at 11.6 percent with a decline in the number of unemployed persons. Retail sales and consumer confidence indices, which serve as an indication of private consumption, weakened this month, but are still high compared to the period since the beginning of the

- 20. crisis. Inflation in the eurozone remained low this month. The ECB did not change eurozone monetary policy this month, but repeated its commitment to low interest rates for a prolonged period, and its readiness to make use of unconventional policy tools. Second quarter data in Japan—high inflation and expectations of negative growth—were affected by the increase in VAT in April, and assessments are that moderate growth will resume at a later time. Developing economies presented a relatively positive picture this month, against the background of low volatility in the markets and continued accommodative policy in Europe and the US. In China, the economy grew by 7.5 percent in annual terms during the second quarter, higher than expectations and in line with the target set by authorities. Oil prices declined by 6.1 percent this month, and the commodities index excluding energy declined by 4.1 percent. The main considerations behind the decision The decision to reduce the interest rate for August 2014 by 0.25 percentage points, to 0.5 percent, is consistent with the Bank of Israel's monetary policy which is intended to return the inflation rate to within the price stability target of 1–3 percent a year over the next twelve months, and to support growth while maintaining financial stability. The path of the interest rate in the future depends on developments in the inflation environment, growth in Israel and in the global economy, the monetary policies of major central banks, and developments in the exchange rate of the shekel. Concurrently the Bank has decided to narrow the interest rate corridor in the credit window and the commercial bank deposit window from ±0.5 percent to ±0.25 percent. The following are the main considerations underlying the decision: There was a decline in the inflation environment this month. Inflation measured over the preceding 12 months declined, as expected, to a level of 0.5 percent, below the lower bound of the target range. The CPI excluding the housing component declined by 0.2 percent over that period. Since the April CPI was published, there has been a decline in inflation expectations for all terms, and short -term expectations approached the lower bound of the target range. Indicators of real economic activity which became available this month indicate continued moderate growth, similar to previous quarters. With that, they refer to the period before the deterioration of the security situation; its moderating effect cannot yet be estimated. Weakness continues in goods exports, against the background of the virtual standstill in world trade and the cumulative appreciation, with moderation in high technology exports. Weakness is also apparent in private consumption over recent

- 21. months. Labor force survey data indicate stability, and the growth in the number of employee posts has halted. The shekel strengthened by 0.8 percent this month in terms of the nominal effective exchange rate, and has appreciated by about 2 percent for the year to date. The real exchange rate is at a level that weighs on growth in the tradable industries—exports and import substitutes, particularly in light of the virtual standstill in world trade. This month, the IMF again reduced its global growth and world trade forecasts for 2014, while leaving the 2015 projections unchanged. In Europe, against the background of continued low inflation, the ECB reiterated its commitment to accommodative monetary policy for an extended period of time, and in the US the tapering process continues, while the assessment remains that the federal funds target rate will not be increased until the middle of 2015. Home prices continued to increase in April–May, and the rate of new mortgages taken out remained elevated, while the risk characteristics of those mortgages continued to decline due to steps taken by the Supervisor of Banks. The number of housing transactions declined sharply. Corporate bond spreads continued to widen, but they are still at a low level. This month, there were net withdrawals from corporate bond mutual funds. The Bank of Israel will continue to monitor developments in the Israeli and global economies and in financial markets. The Bank will use the tools available to it to achieve its objectives of price stability, the encouragement of employment and growth, and support for the stability of the financial system, and in this regard will continue to keep a close watch on developments in the asset markets, including the housing market. - - - - - - - - - - - - - - - - - - - - - - - - The minutes of the monetary discussions prior to the interest rate decision for August 2014 will be published on August 11, 2014. The decision regarding the interest rate for September 2014 will be published at 16:00 on Monday, August 25, 2014.