2. All slides are

taken from this

book which

includes

detailed

explanations of

all concepts.

Available from

Amazon.com

Full color version available at

www.createspace.com/4707238

3. Charitable

Lead Trust

CLAT pays fixed $ annuity

CLUT pays % of trust assets

Charitable

Remainder

TrustCRAT pays fixed $ annuity

CRUT pays % of trust assets

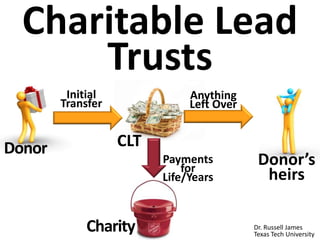

Donor

Charity

Initial

Transfer Anything

Left Over

Payments for

Life/Years

Donor

orheirs

Donor

Charity

Initial

Transfer Anything

Left Over

Payments for

Life/YearsDonoror

heirs

7. The primary

motivation for using a

Charitable Lead Trust

is for tax advantages,

most commonly in gift

and estate taxes

8. Charitable Lead Trusts are less

common than Charitable Remainder

Trusts, but usually involve larger dollar

amounts

$857,297 Average size

$3,165,337

Average size

Source: Split interest trusts, filing year 2011, Lisa Schreiber, IRS Statistics of Income

9. Charitable split-interest trusts by number

Source: Split interest trusts, filing year 2011, Lisa Schreiber, IRS Statistics of Income

6%

93%

1%

Charitable

Lead Trusts

Charitable

Remainder

Trusts

Pooled Income

Funds

11. Charitable split-interest trusts by

distributions to charity

Source: Split interest trusts, filing year 2011, Lisa Schreiber, IRS Statistics of Income

37%

62%

1%

Charitable

Lead Trusts

Charitable

Remainder

Trusts

Pooled Income

Funds

12. 0%

10%

20%

30%

40%

50%

60%

70%

CRT

CLT

Charitable beneficiary distribution sharebytype

This may reflect

greater CLT use of

private foundations

as charitable beneficiaries

Source: Split interest trusts, distributions of principal

and interest combined, filing year 2011, Lisa

Schreiber, IRS Statistics of Income

13. Donor

Charity

Initial

Transfer Anything

Left Over

Payments for

Life/Years

Donoror

heirs

CLT

Payments may be for

life or any time

period and can be for

any fixed dollar

(CLAT) or ongoing %

(CLUT) amount

Donor

Charity

Initial

Transfer Anything

Left Over

Payments for

Life/YearsDonoror

heirs

CRT

Payments may be for

life or up to 20 years,

and must be 5% to

50% of initial (CRAT)

or ongoing (CRUT)

trust assets

14. Donor

Charity

Initial

Transfer Anything

Left Over

Payments for

Life/Years

Donoror

heirs

CLT

The trust is not tax

exempt, so the trust

(non-grantor CLT) or

donor (grantor CLT)

must pay taxes on

trust earnings

Donor

Charity

Initial

Transfer Anything

Left Over

Payments for

Life/YearsDonoror

heirs

CRT

The trust is tax

exempt, so there are

no immediate taxes

on trust earnings

17. Donor

Charity

Initial

Transfer Anything

Left Over

Payments for

Life/Years

Donor’s

heirs

Projected

Value of

Remainder

Gift taxes are

not paid on the

ACTUAL

remainder that

eventually goes

to the heirs

Gift taxes are paid

on the present

value of the

PROJECTED

remainder going

to the heirs

19. Donor

Charity

Initial

Transfer Anything

Left Over

Payments for

Life/Years

Donor’s

heirs

Projected

Value of

Remainder

If actual growth is

greater than the §7520

rate, the ACTUAL

remainder will be

greater than projected

The

PROJECTED

remainder assumes

investment growth

at the §7520 rate

20. Gift tax on the transfer less the projected

value of charity’s payments

Value of

projected

payments

to charity

(not taxed)

Value of

projected

remainder

to family

(taxed)

22. Find the §7520 rate

http://www.irs.gov/Businesses/Small-Businesses-&-Self-

Employed/Section-7520-Interest-Rates

Multiply payment by annuity

factor in IRS Pub. 1457http://www.irs.gov/Retirement-Plans/Actuarial-Tables

Value of CLAT

payments

23. Find the §7520 rate

http://www.irs.gov/Businesses/Small-Businesses-&-Self-

Employed/Section-7520-Interest-Rates

Can choose

current or

one of last

two month’s

rate

$1MM/yearfor

11yearsCLAT

on10/31/13

Aug 2.0%

Sept 2.0%

Oct 2.4%

25. Find the §7520 rate

2.0%http://www.irs.gov/Businesses/Small-Businesses-&-Self-

Employed/Section-7520-Interest-Rates

To get the

highest

annuity

valuation

[lowest gift

tax]

select

Sept 2.0%

$1MM/yearfor

11yearsCLAT

on10/31/13

26. Table B – Annuity interest for a Term Certain

Interest at 2.0 Percent

Years Annuity Income Interest Remainder

8 7.3255 0.195737 0.853490

9 8.1622 0.211507 0.836755

10 8.9826 0.195737 0.820348

11 9.7868 0.211507 0.804263

12 10.5753 0.195737 0.788493

Find the §7520 rate

2.0%www.irs.gov/Businesses/Small-Businesses-&-Self-Employed/Section-

7520-Interest-Rates

Multiply annual payment by

annuity factor in IRS Pub. 1457

$1MM X 9.7868www.irs.gov/Retirement-Plans/Actuarial-Tables

$1MM/yearfor

11yearsCLAT

on10/31/13

27. Find the §7520 rate

2.0%www.irs.gov/Businesses/Small-Businesses-&-Self-Employed/Section-

7520-Interest-Rates

Multiply annual payment by

annuity factor in IRS Pub. 1457

$1MM X 9.7868www.irs.gov/Retirement-Plans/Actuarial-Tables

Value of annuity

$9,786,800

If annuity

pays more

than

annually, add

adjustment

factor from

Table K

$1MM/yearfor

11yearsCLAT

on10/31/13

28. Donor

Charity

Initial

Transfer Anything

Left Over

Payments for

Life/Years

Donor’s

heirs

Projected

Value of

Remainder

If actual

growth is 8%,

the ACTUAL

remainder will

be $6,670,903

Transfer $10MM to a CLAT with

$1MM/year charitable annuity

for 11 years ($9,786,800 value),

pay tax on $213,200 present

value of PROJECTED

remainder to kids

29. A CLT can “zero out” gift and estate

taxes by setting the

non-charitable

value at zero

30. Find the §7520 rate

2.0%www.irs.gov/Businesses/Small-Businesses-&-Self-Employed/Section-

7520-Interest-Rates

Multiply annual payment by

annuity factor in IRS Pub. 1457

$1,021,785 X 9.7868www.irs.gov/Retirement-Plans/Actuarial-Tables

Value of annuity

$10,000,005

If annuity

pays more

than

annually, add

adjustment

factor from

Table K

$1,021,785/

yearfor11

yearsCLATon

10/31/13

31. Donor

Charity

Initial

Transfer Anything

Left Over

Payments for

Life/Years

Donor’s

heirs

Projected

Value of

Remainder

If actual

growth is 8%,

the ACTUAL

remainder will

be $6,308,281

The PROJECTED remainder

of $10MM at 2% §7520 with

$1,021,785/year charitable

payments for 11 years is $0,

resulting in $0 gift taxation

33. If the

charitable gift

(or bequest)

was already

planned, the

zeroed-out

CLAT

(or zeroed-out

testamentary

CLAT)

provides a no

cost chance at

tax-free

transfers to

family

35. A step-CLAT increases payments

to charity by a fixed

percentage, paying

less in early

years and

more in

later years

Year 5

$207

(+20%)

Because more

assets stay in longer,

more growth can occur,

leaving more for family

Year 6

$249

(+20%)

Year 7

$299

(+20%)

Year 8

$299

(+20%)

37. Donor

Charity

Initial

Transfer Anything

Left Over

Payments for

Years

Donor’s

heirs

Projected

Value of

Remainder

If ACTUAL length of

life is less, the ACTUAL

remainder will be greater

than projected

If payments are for life,

the PROJECTED

remainder is based on

NORMAL life

expectancy

38. The measuring life/lives

must be donor, any

ancestor of the

remainder beneficiaries,

or spouses of either.

Measuring life

cannot be used

“if there is at

least a 50 percent

probability that the

individual will die within

1 year” unless person

actually lives at least 18

months.

39. Your son called to tell you that you are the

measuring life for his CLT, so make sure to

live slightly over 18 more months

40. While you are waiting…

• A CRT can be used to

generate current

income while waiting

for a CLT to mature

• Multiple CLTs can be

staggered to end at

different times to

smooth the transfer

• CLTs are often

established at death

(testamentary)

43. Distributing CLAT Shares Early

IRS has approved early

termination when the

CLAT immediately pays all

future required payments

(undiscounted) to the

charityPLRs 200225045, 199952093, 9844027

44. Issues for Generation Skipping Transfers

• CLATs (not CLUTs) taxed on

projected and actual amount

transferred to skip persons

• If charity can be changed, tax is

recipient liability, so trust

payment of tax creates more

tax

45. Growth can also avoid taxation using a

non-charitable plan (Grantor Retained

Annuity Trust), but the creator must outlive

the term of the GRAT for it to work

46. I want to donate

income from my

assets, but I am

already over the

income

percentage limit

for deductions

47. Donor

(Non-Grantor) CLT

taxed on income

Charity

Initial

Transfer

Anything

Left Over

Payments

for

Life/Years Donor’s

heirs

Charitable

deductions

to CLT with

no income

limitationsCLT can also pay

out any income in

excess of annuity

or unitrust amount

49. Grantor CLT

• Future income is

taxed to donor

• Donor gets a

deduction

• Remainder included

in donor’s estate

(typically returns to

donor)

Non-Grantor CLT

• Future income is

taxed to trust

• Trust deducts

payments to charity

• Remainder not

included in donor’s

estate

50. I give regularly, but

I need a giant

deduction

to offset a

big spike in income

this year

(e.g., due to a sale,

Roth conversion, bonus,

etc.)

51. In a grantor CLT,

the donor

commits to

future gifts and

receives an

immediate tax

deduction for

the present

value of these

gifts

53. Donor

Charity

Initial

Transfer Anything

Left Over

$10,000 Payments

for 20 years

Funding $10,000/year gifts through a 20-year

grantor CLAT (returning remainder to donor)

creates an immediate deduction of

• $163,514 at 2% §7520 rate

• $98,181 at 8% §7520 rate

55. Grantor CLTs

• Donor gets a

deduction

• Future income is

taxed to donor

• Remainder included

in donor’s estate

(often returns to

donor)

Non-Grantor CLTs

• Future income is

taxed to trust

• Trust deducts

payments to charity

• Remainder not

included in donor’s

estate

56. Grantor CLTs

• Donor gets a

deduction

• Future income is

taxed to donor

• Remainder included

in donor’s estate

(often returns to

donor)

Non-Grantor CLTs

• Future income is

taxed to trust

• Trust deducts

payments to charity

• Remainder not

included in donor’s

estate

CLT “Defective Grantor Trust” (aka “SuperTrust”)

57. CLT“Defective Grantor Trust”(aka“Super Trust”)

Non-Grantor CLTs

• Future income is

taxed to trust

• Trust deducts

payments to charity

• Remainder not

included in donor’s

estate

A Grantor CLT for

Income Tax purposes.

A Non-Grantor CLT for

Estate Tax purposes.

Grantor CLTs

• Donor gets a

deduction

• Future income is

taxed to donor

• Remainder included

in donor’s estate

(often returns to

donor)

58. How does it work?

• Estate tax and

income tax grantor

trust definitions are

not precisely

identical

• If donor keeps a right

to get trust property

by substituting other

property of equal

value, it causes

grantor treatment

for income tax, but

not estate tax

59. The “Defective Grantor

Trust” or “Super Trust”

attempts to mix

characteristics of the

two kinds of CLTs. It

may work, but lacks

conclusive authority.

Less aggressive

planners might leave

this superhero in the

phone booth.

61. CLTs must follow same rules as

private foundations

for self-dealing, taxable expenditures, jeopardizing

investments, and excess business holdings

62. A GRANTOR CLT

may be a subchapter S

corporation

shareholder because

donor is treated as

stock owner

NON-GRANTOR CLT

should not hold

subchapter S shares,

because trust is treated

as the owner

(allowed only when ESBT election

eliminates charitable deductions)

Subchapter S-Corp Stock

63. Unrelated business

income (e.g., from

debt-financed

property or actively

managing business) is

allowed.

But in a non-grantor

CLT, giving this income

to charity is

deductible only at

50% (to public

charity) or 30% (to

private foundation).

65. Help me

HERE

convince my bosses that continuing to build and

post these slide sets is not a waste of time. If

you work for a nonprofit or advise donors and

you reviewed these slides, please let me know

by clicking

66. If you clicked on

the link to let

me know you

reviewed these

slides…

Thank

You!

67. This slide set is from the curriculum for

the Graduate Certificate in Charitable

Financial Planning at Texas Tech

University, home to the nation’s largest

graduate program in personal financial

planning.

To find out more about the online

Graduate Certificate in Charitable

Financial Planning go to

www.EncourageGenerosity.com

To find out more about the M.S. or

Ph.D. in personal financial planning at

Texas Tech University, go to

www.depts.ttu.edu/pfp/

Graduate Studies in

Charitable Financial Planning

at Texas Tech University