2. ACCOUNT

An account is a summarized record of transactions

relating to a particular person, asset, liability,

particular head of expense or income

recorded at one place.

• Types of Account-

Personal Account

Impersonal Account

Real Account

Nominal Account

3. PERSONAL ACCOUNTS

This account represents a person and group of persons with whom business deals.

These accounts are classified into following three categories:

a) Natural Person's Account: Accounts relating to individual human beings.

E.g. Rajesh’s A/c, Sumit's A/c, Sushma's A/c, Vaibhav’s A/c etc.

b) Artificial Person's Account: Artificial persons means includes accounts of

organizations, associations which are created by law,

E.g. Bank of Maharashtra A/c, ABC & Co A/c, Recreation Club A/c.

c) Representative Personal Account: These Accounts represent a certain person or

group of person in business dealing.

Accounts relating to outstanding and prepaid items are called representative

personal account

E.g. Outstanding Rent A/c, Income received in advance A/c, Prepaid Wages A/c

etc.

4. IMPERSONAL ACCOUNT

Impersonal Accounts are classified into following two categories;-

1. Real Accounts: This account represents assets and properties owned by

the business.

The following are the types of Real Account.

a) Tangible Real Account: Tangible real account means the Assets and

properties, which can be seen, touched and felt.

e.g. Machinery A/c, Motor Car A/c, Stock of Goods A/c etc.

b) Intangible Real Account: Intangible Real account means assets which

cannot be seen, touched, or felt but they can be measured in terms of

money

e.g. Goodwill A/c, Patents A/c, Trademark A/c, Copyright A/c etc.

5. 2. Nominal Accounts: The account of expenses, losses, income and

gains are called as Nominal accounts

e.g. Wages A/c, Stationery A/c, Salary A/c, Depreciation A/c Commission

Received A/c, Discount Received A/c etc.

Personal account

• Customers

• Debtors

• Creditors

• Drawings

• Capital

• Companies

• Corporations

• Partnerships

• Government bodies

• Trusts

Real account

• Cash

• Accounts

receivable

• Inventory

• Prepaid expenses

• Land

• Buildings

• Equipment

• Intangible assets

(e.g., patents,

copyrights,

goodwill)

Nominal account

• commissions

• advertising

• shipping

• salaries

• rent

• utilities

• Depreciation expense

• Interest expense

• losses from fires,

floods, and other

unforeseen events.

7. IT AFFECTS THE CAPITAL ALWAYS

• Expenses: cost incurred in acquiring an asset or service in

the form of outflow of asset or incurrence of liability. like

purchase account

• Losses: decrease in equity from incidental transactions

except those that result from expenses or distribution to

equity holders. like loss on sale of investment or assets

• Income: increase in economic benefit in the form of inflow

of assets or decrease of liabilities that result in increase in

internal equity. like sales account

• Gain: increase in equity from incidental transactions except

those that result from revenue or investment by equity

holders. like profit on sale of investment or assets

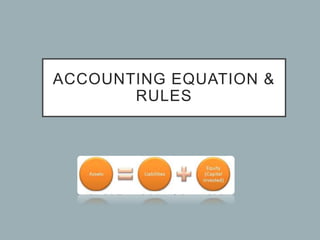

8. ACCOUNTING EQUATION

• A mathematical expression, which shows that the

assets and liabilities of a firm are equal, is known

as accounting equation.

• An accounting equation is based on dual aspect

concept which states that every transaction has two-

fold aspects.

• An accounting equation always holds true with every

change that occurs due to the reason that it is based

on the dual concept of accounting

9. • The equation signifies that the assets of a business are

always equal to the total of its liabilities and capital

(owner’s equity).

• Accounting equation is expressed as

ASSETS= CAPITAL+LIABILITIES

• The above equation can also be presented in the

following forms-

CAPITAL =ASSETS - LIABILITIES

LIABILITIES = ASSETS – CAPITAL

10. STEPS INVOLVED IN DEVELOPING AN

ACCOUNTING EQUATION

STEP 1 Ascertain the variables(i.e. assets, liabilities or

capital) involved in a transaction.

STEP 2 Find out the effect (in terms of increase or

decrease)of a transaction on assets ,capital or liabilities.

STEP 3 Show the effect(i.e., add or deduct)on the

appropriate side of an equation and ensure that the total

of right hand side is equal to the total of left hand

side.

i.e. A=L+C.

11. REMEMBER FOR ACCOUNTING EQUATION

1. every transaction affects atleast two accounts

2. basic accounting equation is :

Assets= Liabilities + Capital

3. All expenses/ Losses-----

4. All income/gains------ included in capital

5. Drawings ------deducted from capital

6. Profit= Opening capital+ Additional capital- drawings-

closing capital

7. Purchase or sale of goods---- treated as stock (assets)

8. adjustment in capital will be made for current

accounting period only.

12. TRANSACTIONS

(SIMPLE ENTRIES)

1. started business with cash Rs.1,00,000

2. purchased goods on cash Rs. 30,000

3. sold goods costing Rs. 20,000 for cash

4. sold goods on credit Rs. 10,000

5. goods of Rs.10,000 destroyed by fire

6. paid Rs. 20,000 to creditors

7. debtors paid Rs. 10,000

8. commission paid Rs. 10000

Answer : Balance of both sides--- ???

13. TRANSACTIONS

(COMPOUND ENTRIES)

1. started business with cash 2,00,000 & bank

1,00,000

2. purchased goods on cash 40,000 & on credit

25,000

3. sold goods costing 30,000 for cash and 40,000

for credit

4. paid 21,000 to creditors in full settlement

5. sold goods costing 10,000 for 15,000 on credit

6. Paid interest on loan 1200

7. Introduced additional capital 50,000

8. debtors paid 37,000 in full settlement

9. withdrawn from bank 6,500 for personal use

Answer : Balance of both sides--??

14. MOST IMPORTANT

• outsanding expenses-- due but not paid---

liability

• prepaid expenses--- paid in advance--- asset

• accrued income-- earned but not received---

asset

• unearned income-- received in advance---

liability

15. TRANSACTION

1. started business with cash 2,00,000

2. rent for the month is 2000 per month & rent paid is 20,000

3. rent for the month is 2000 per month & rent paid is 30,000

4. commission is 3000 per month & received is 30,000

5. commission is 3000 per month & received is 50000

Answer: Balance of both sides at the end is 2,42,000

16. SOLUTION

paid 20000 so deducted from cash & effect on capital (-24000 & liability 4000 as outstanding

expenses)

(2000*12=24000= rent of year) & ( deduction in capital with whole amount of this accounting

period only)

paid 30000 so deducted from cash & effect on capital (-24000 & assets 6000 as prepaid

expenses)

(2000*12=24000= rent of year) & ( deduction in capital with whole amount of this accounting

period only)

After 3rd entry balance of both side is 1,56,000

received 30000 so added in cash & capital 36000 (3000*12) & 6000 (accrued income on assets)